Bridging loans are meant to reduce the financial burden in the transition when you buy and sell a property simultaneously.

This short-term bank loan allows you to pay the downpayment of your new property before receiving the sale proceeds from the previously sold property.

This is useful when you’ve already found the perfect home for yourself and wish to secure the listing before anyone else does. However, it is likely that you may not have the cash on hand and have not received the cash from selling your current property.

Illustration of how a Home Bridging Loan works

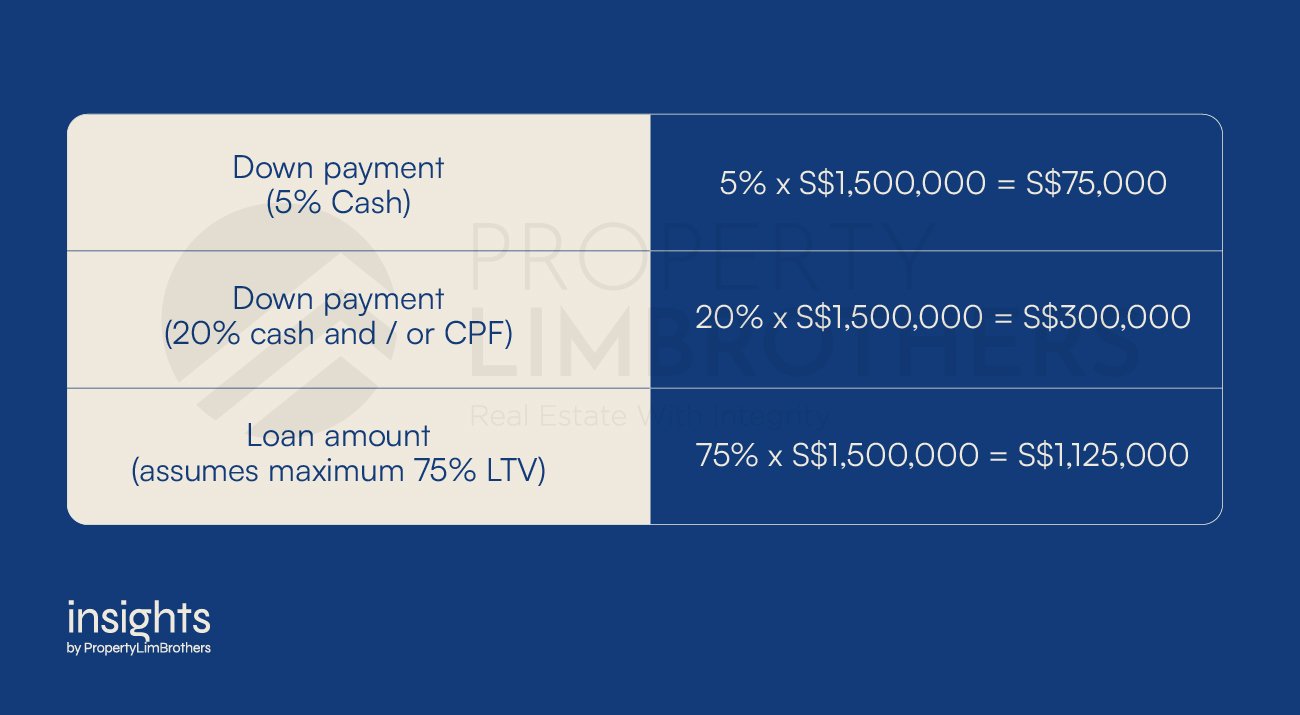

Assuming you are in the process of selling your existing HDB to purchase a resale condominium but will only be receiving the sale proceeds after 4 months.

In order to finance the purchase of a $1.5 million resale condominium

In order to secure the purchase, you would have to make the down payment, assuming that you have insufficient cash and/or CPF to make the 20% down payment, you would be able to still go ahead with securing the property by taking up a bridging loan of S$300,000 to make up for the shortfall. Provided that the sale proceeds of the sale of your previous property is more than S$300,000.

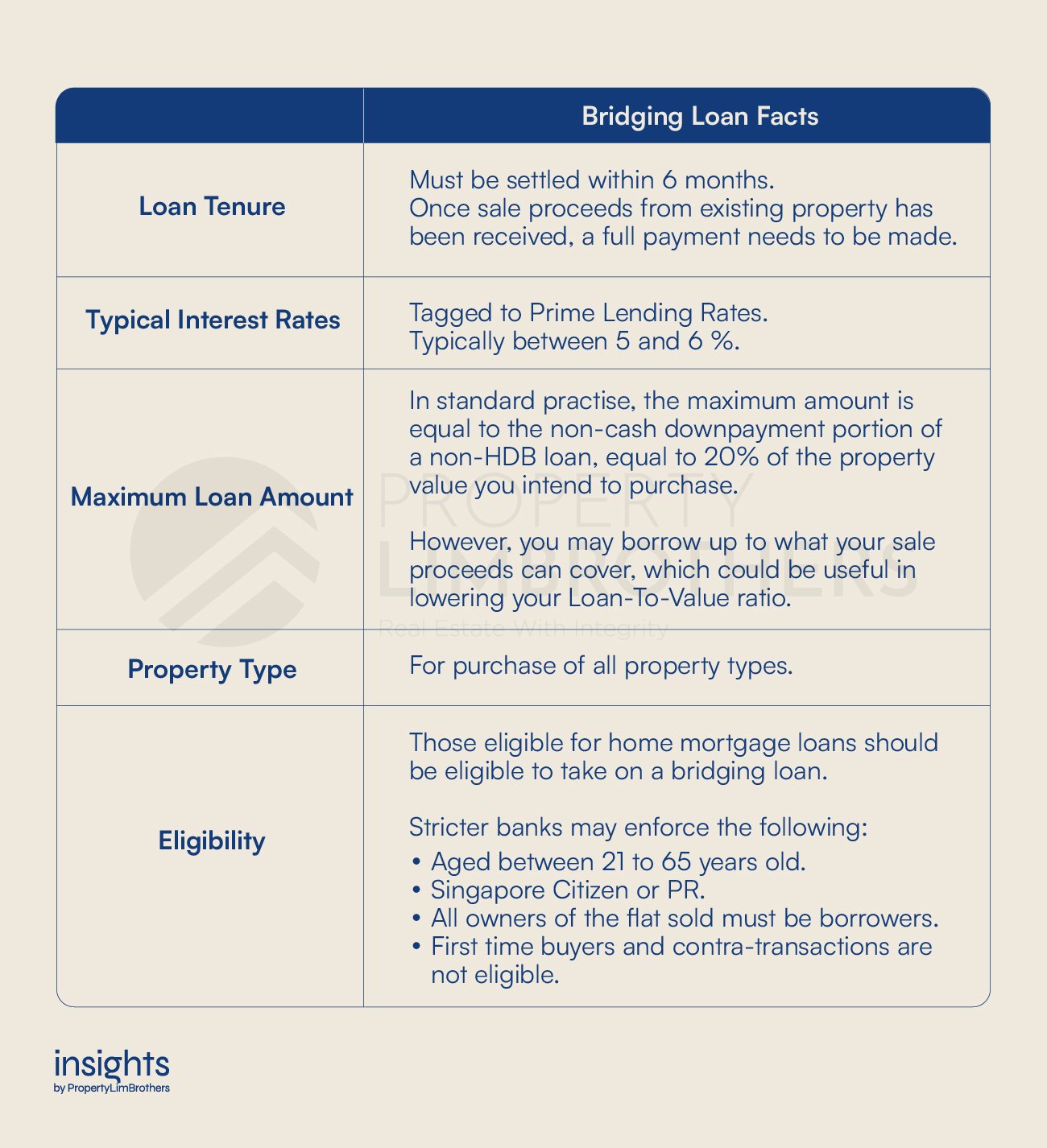

Bridging Loan Facts

Types of Bridging Loans

Capitalised Interest Bridging Loan

Capitalised interest bridging loan covers the full amount of the new home you are intending to purchase. Repayment of the bridging loan only starts after selling your current property, in this way you will not be paying for two loans at the same time, in other words, you will not be paying for the current home’s mortgage loan and the bridging loan at the same time. This could be helpful in reducing your financial responsibilities during this time of transition.

Simultaneous Payment Bridging Loan

Opposite of Capitalised interest bridging loans are simultaneous payment bridging loans whereby you need to, as the name suggests, simultaneously repay your home loan and bridging loan. This could be a little bit more fiscally stressful for some.

When Should I use a Bridging Loan

Quite simply if you do not have enough cash and/or CPF to cover the down payment on your new property, you would need a bridging loan, vice versa.

However it could be your preference to take a bridging loan to conserve your cash reserves for emergency situations. However by doing so you will be incurring the cost of interest on the bridging loan.

Things to consider when taking a Bridging Loan

Secured Debt: Property acting as collateral

Your property will be used as the collateral for your loan repayment. Hence it is paramount that you have made sure that you have the capacity to repay the loan in a timely fashion.

What happens if my property sale does not go through?!

Not properly planning could result in this recipe for disaster, for whatever reason that your old property does not proceed there will be exit clauses made by the bank, resulting in, typically, a penalty that is to be paid by the borrower.

Hence before signing on a bridging loan, always check what are the exit terms and conditions which will vary from bank to bank. and take these clauses into consideration when selecting a suitable loan.

Using CPF for a bridging loan

While you may utilise the refunded CPF from the sale of your property to repay the bridging loan, the interest portion needs to be serviced with cash.

Still unsure how to go about your Simultaneous Buy and Sell?

If you’re still unsure how you should go about with upgrading or downgrading your current property portfolio feel free to contact us for a non-obligatory consultation with our Inside Sales Team!