There are many important aspects people look at when considering a home. Apart from whether they are getting value for money, or if the transacted volumes are high, the amount of lease left is an obvious thing to look out for. Depending on the needs of the buyer, the required and expected lifespan of the home will differ.

In this article, we touch on the essence of Bala’s Curve, why it matters, and how we use it in our MOAT Analysis. While the importance of lease might be self-explanatory to many, we hope to go a little deeper into the relationship between lease & value, and who benefits most from it.

The Essence of Bala’s Curve

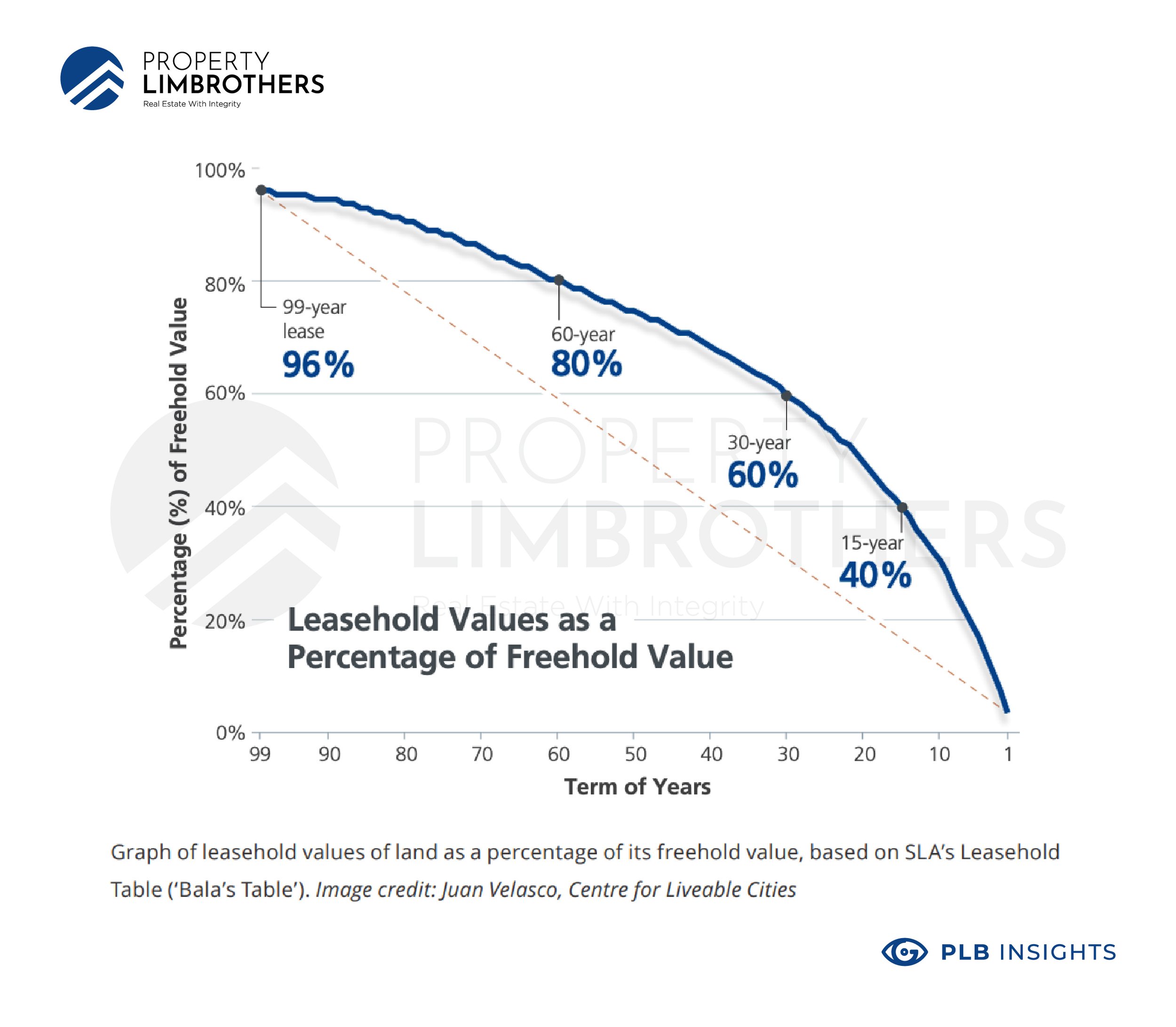

When comparing leasehold with freehold properties, it is sometimes like comparing an apple with an orange. The main purpose of Bala’s Curve is to find a way to compare the value of leasehold and freehold properties. If you have to remember just one thing from this section, just know that leasehold values (as a percentage of freehold values) tend to fall faster as they age. The theory is that the older the leasehold property is, the depreciation accelerates.

Our friends at 99.co did a great job on explaining the Bala’s Curve, its history and its uses. You can take a read if you want an introduction on it and how the discount rate works over time. To demonstrate this visually, we refer to a chart provided by the Centre for Liveable Cities (CLC).

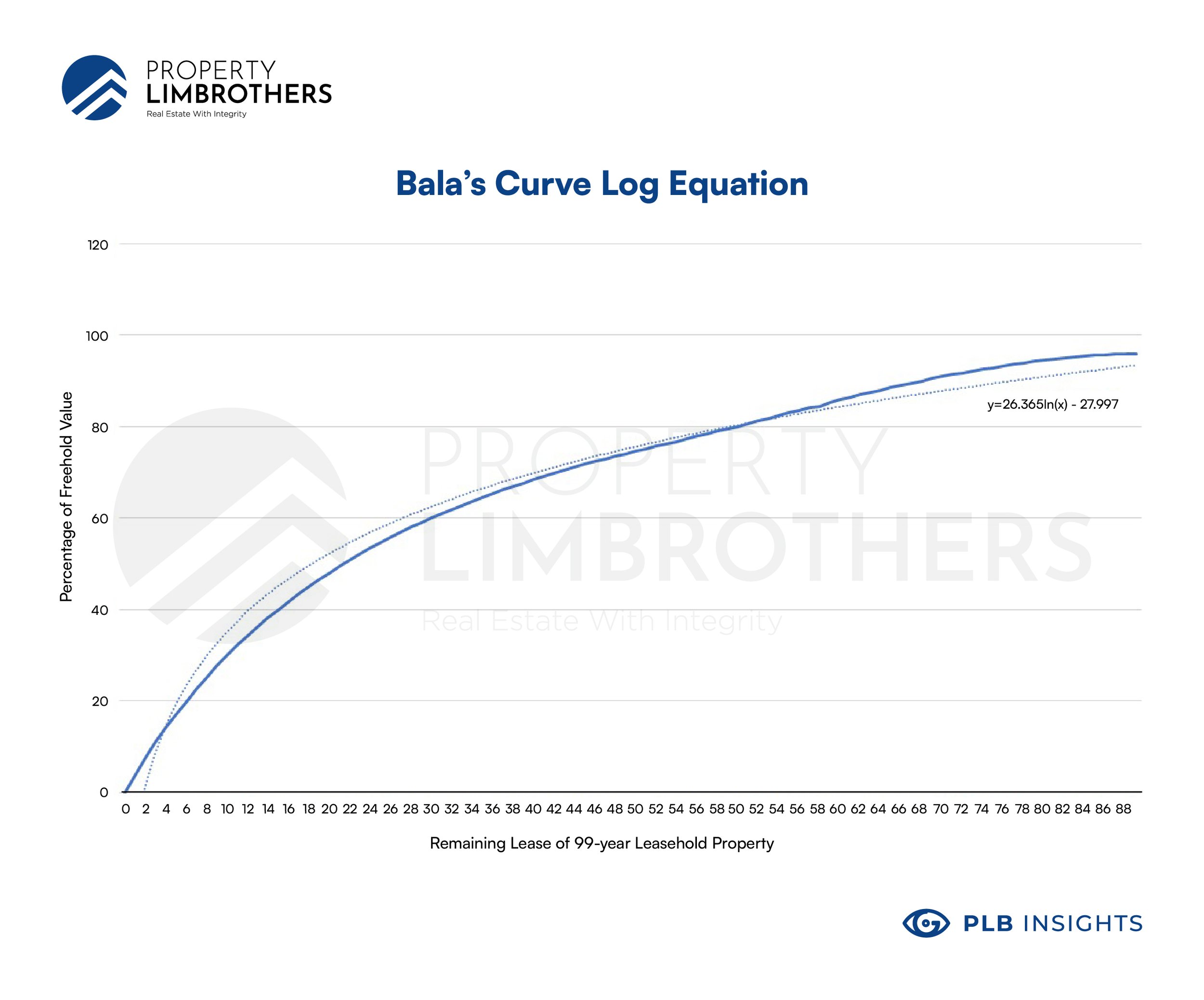

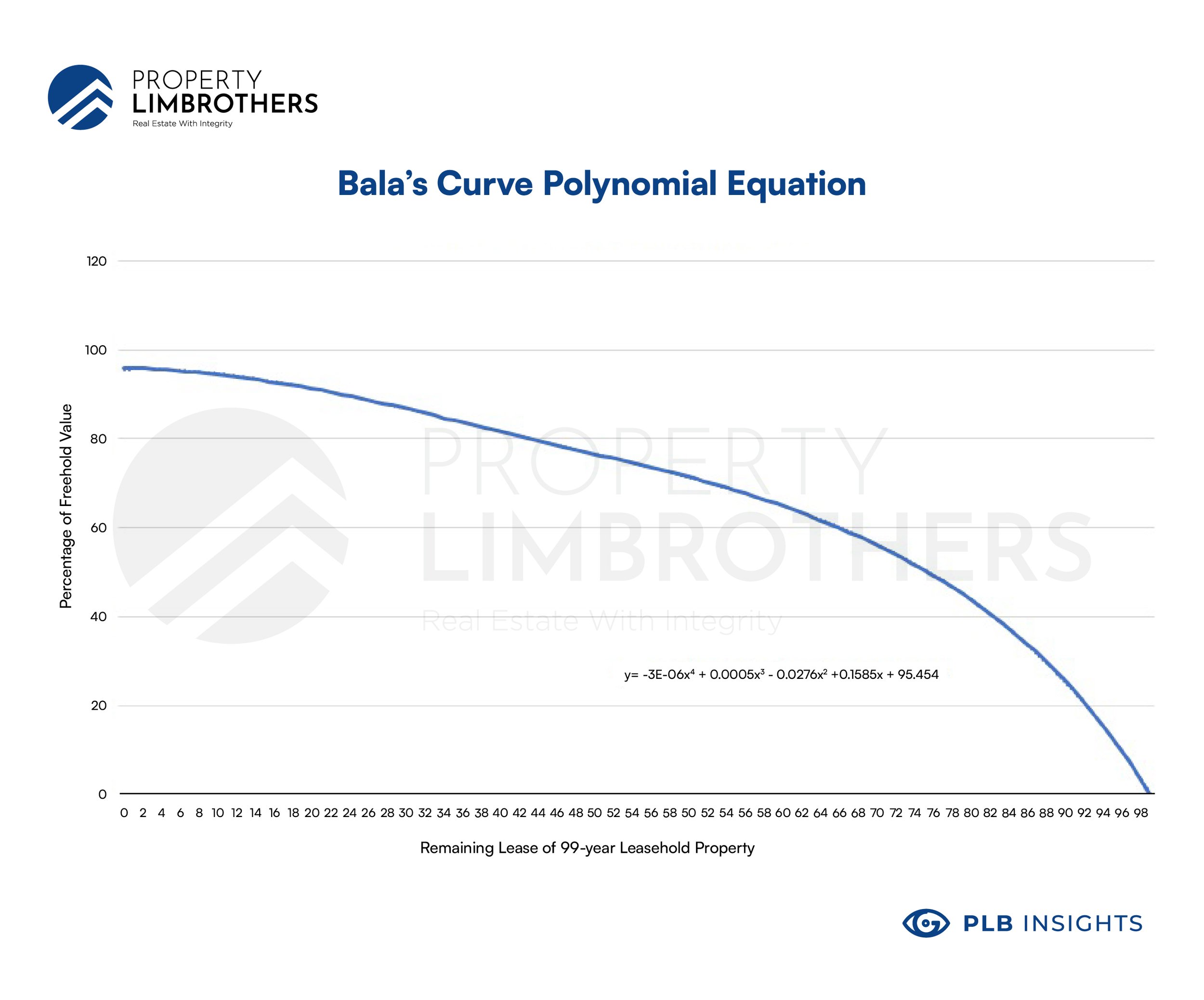

Fun fact for quants, this is basically the reflection of an exponential curve on the x-axis. We have cracked the equation to Bala’s Curve. (Our equations are the best fit lines, and might not be the exact one that government and financial institutions use). Here are the logarithmic and polynomial functions. We plot it as a function of remaining lease (logarithmic) and as a function of age (polynomial).

You can use our polynomial function in the above chart to take a peek at how much your property would be worth against its theoretical freehold counterfactual. The ultimate premise of Bala’s curve is that freehold properties command a premium above their leasehold counterparts. This boils down to people’s preference for properties that can last beyond their lifespan, as a multi-generational asset.

A caveat we want to raise here is that the notion of a multi-generational asset has a possibility of becoming less popular with the next few generations. Younger couples and retirees are starting to see the value of lower lease properties in meeting their own needs. Stories of young couples going for lower lease projects might hit the headlines more often. While this might not be optimised for investment returns, the increase in demand for lower lease properties might weaken the relationship between the value of leasehold and freehold properties. If the value of leasehold properties catch up to freehold ones (especially for lower lease properties), then we would see the depreciation curve become less steep as properties get older.

We’d like to caution that the Bala’s curve is just an equation. It might not necessarily track the conditions on the ground. Nor does it reflect the actual value comparison between freehold and leasehold properties. It is simply a rule-of-thumb to apply a quick comparison between the two.

Why does Bala’s Curve matter?

Bala’s curve still matters despite the caveat we mentioned because the demand for low lease properties is coming from a small niche population as of now. Bala’s curve would matter the most to investors. With a limited time horizon and concern about the rate of return, Bala’s curve would serve to give investors a heads up on the depreciation of leasehold properties. And if the property is too old, hence presenting an unacceptable depreciation risk moving forward.

The depreciation of old leasehold properties is driven by other factors apart from the property being set to expire soon. The first being the difficulty in obtaining a loan from the bank to purchase the property. If the bank is not confident in collateralising the property, you may be presented with a lower Loan-to-Valuation, or a shorter loan tenure. This would end up pushing buyers to draw out more cash from their pockets to fund the purchase. Or find themselves with higher mortgage payments.

Investors might see this pose a huge risk to exit. It will take additional time and effort to exit such properties. You would need to find a niche population, like the one we mentioned earlier. A group of buyers that are fine with the low remaining lease and see that it fits their personal needs. This group is currently small, nascent, but potentially growing over the next few decades.

Another important reason we should look at Bala’s curve is because of the en bloc risk. En blocs are not always a good thing. If you have been a long time owner of the property, an en bloc might be great news for getting a good deal when cashing out. This might not be true for some investors who entered at an unlucky time. If the en bloc happens within 3 years of your property purchase, you would be liable to pay the Seller’s Stamp Duty. This could really hurt your investment returns, likely resulting in a loss.

It is for these reasons that investors avoid low lease projects. If you are looking for a quick comparison between projects. Bala’s curve would help to give investors a warning sign on which properties have a higher risk based on their remaining lease.

How do we use Bala’s Curve in the MOAT Analysis?

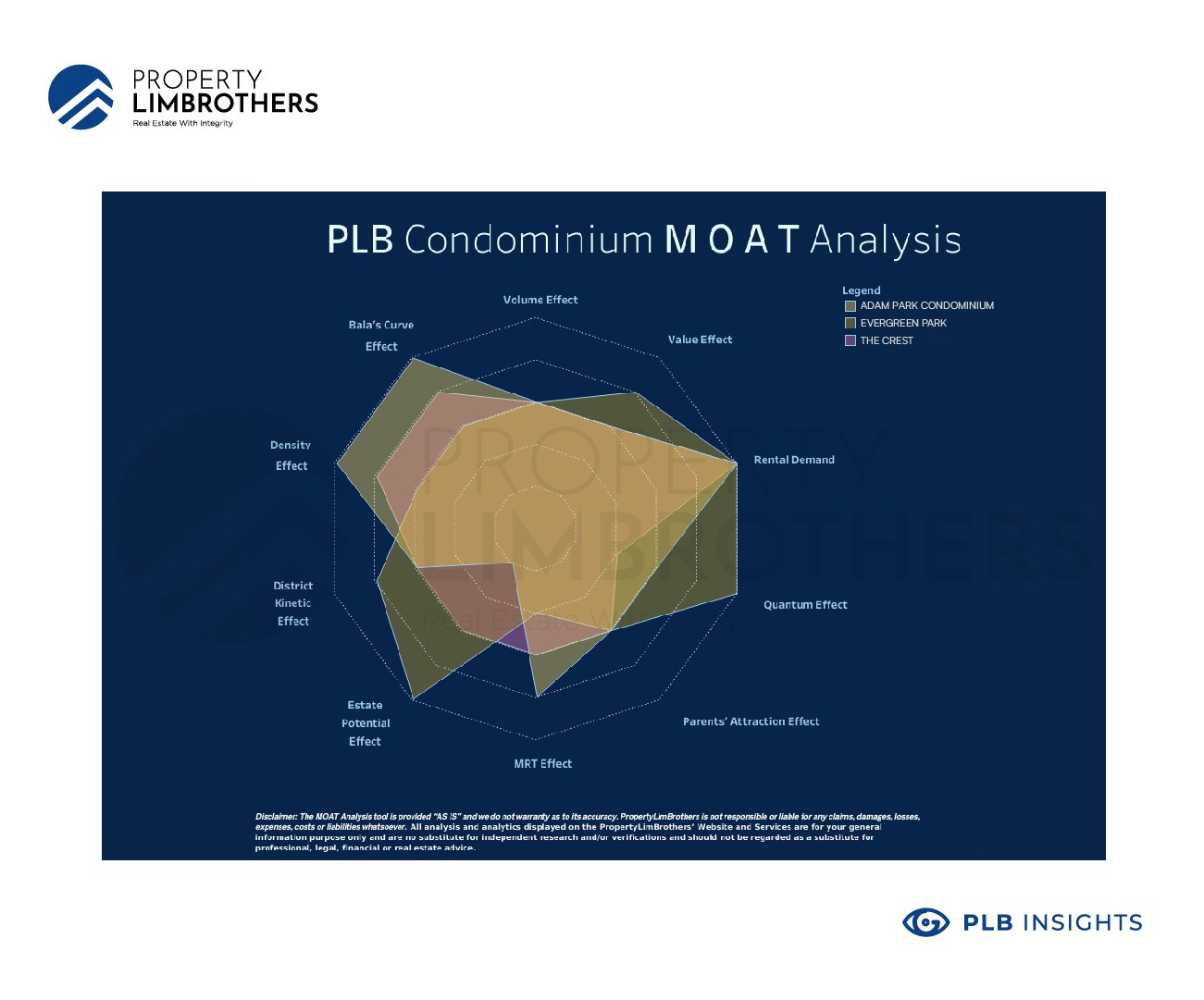

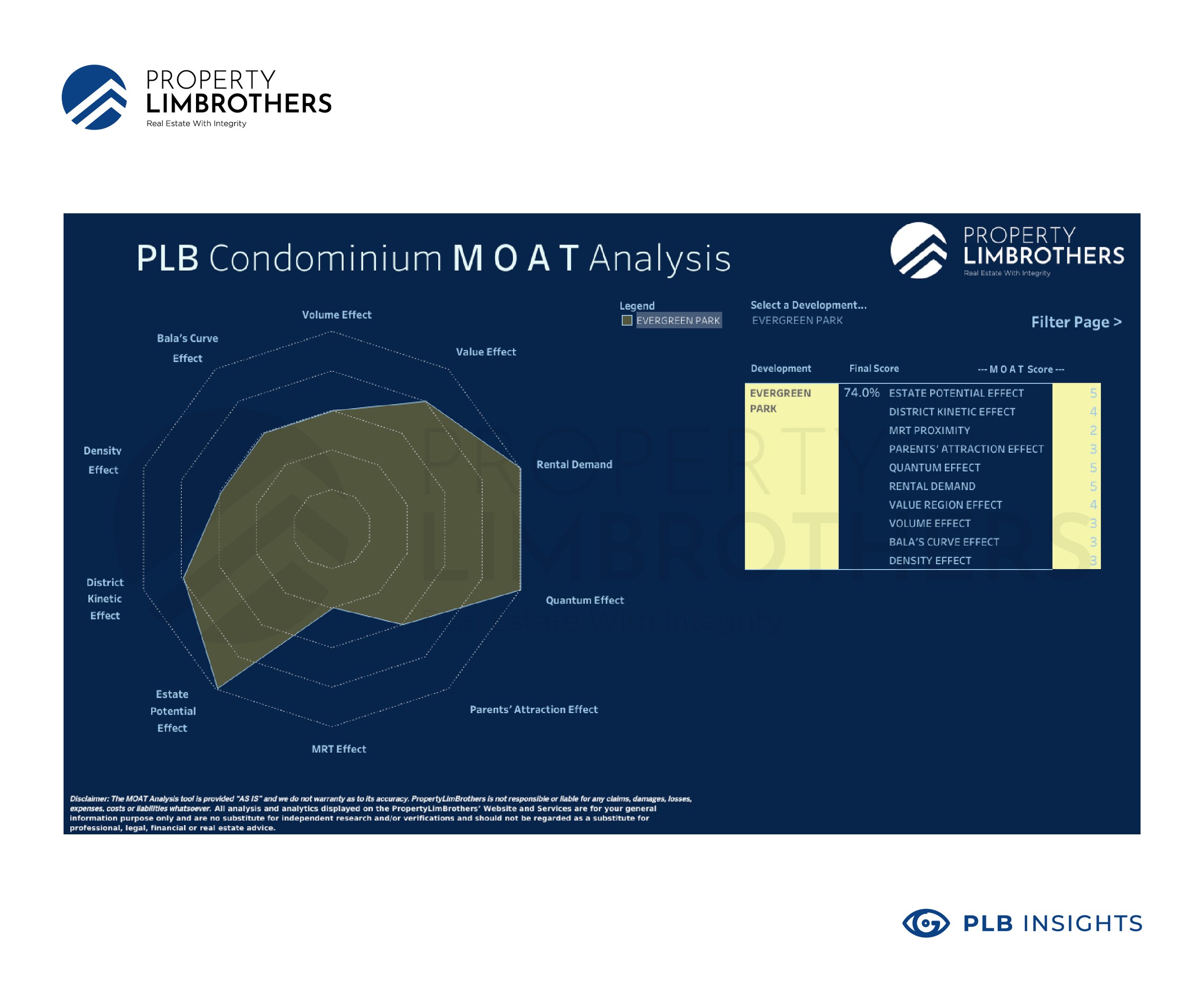

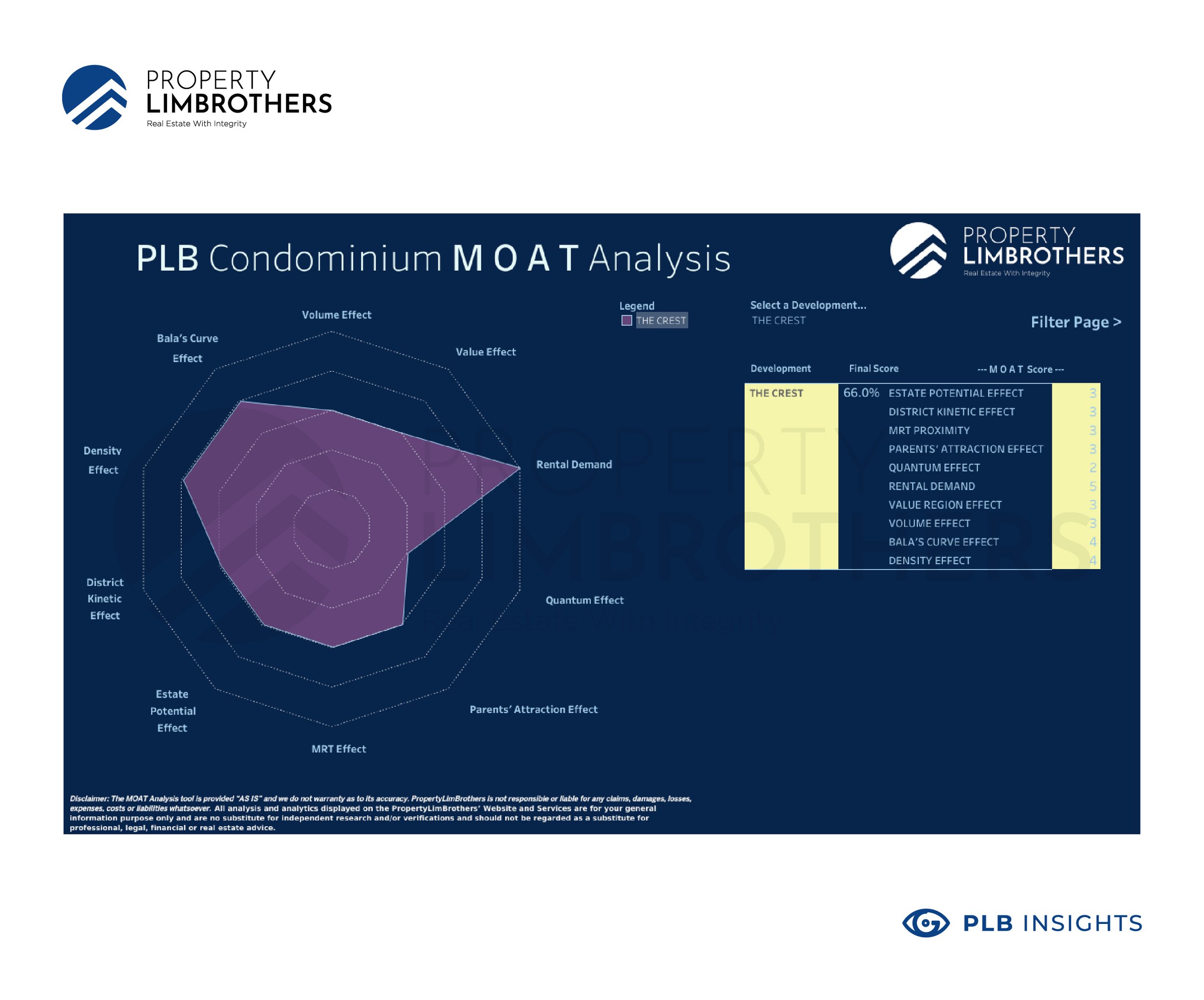

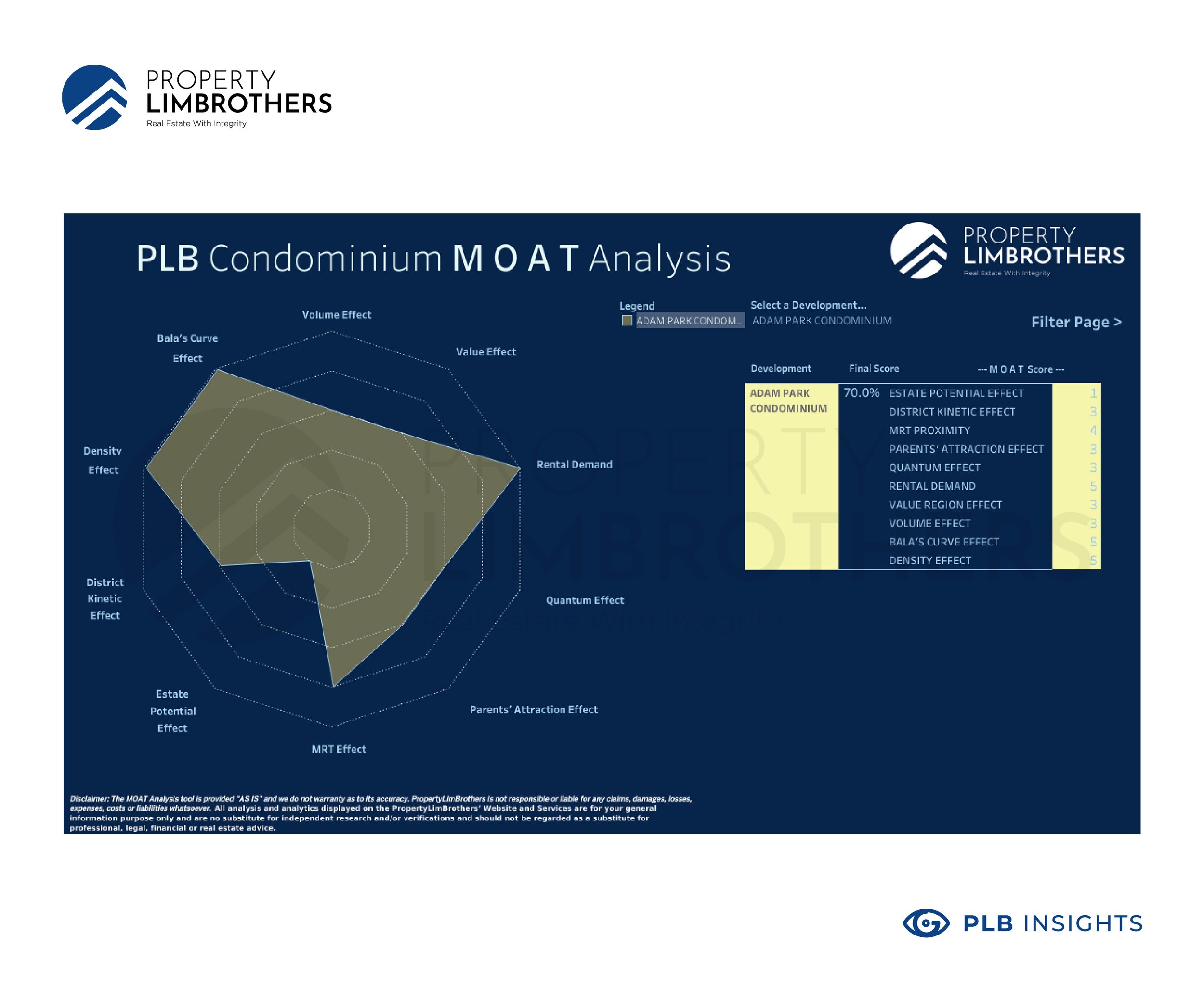

For demonstration purposes, we compare three different properties to illustrate Bala’s curve in the context of our MOAT Analysis. We look at Adam Park Condominium, The Crest, and Evergreen Park. Adam Park is a freehold condominium in District 11 with 118 units. The Crest is a 99-year leasehold (from 2012) condominium with 469 units in District 3. Last but not least, Evergreen Park is a 99-year leasehold (from 1995) condominium with 394 units in District 19.

In the MOAT Analysis, properties are graded on the scale of 5 points for each category. For Bala’s curve, we account for the non-linear relationship we describe in the first section within the 5-point scale. So you do not have to bend your mind backwards to calculate the exact depreciation risk by the exact equation.

In this exercise, we wish to give an example of how low lease projects might not equate to a worse property right off the bat. You would need to look at other factors to see how it balances out the pros and cons of the property. For Evergreen Park, it has the lowest MOAT score of 3 as compared to the two other condos. However, it has the highest total MOAT score of 74%. This is because of the high performance on Rental Demand, Quantum Effect, and Estate Potential Effect. We will cover these effects and what they mean in the following weeks.

For a property investor looking at this, you might want to consider if the perks of owning the property outweigh the low lease issue (and other factors that are not performing such as MRT Distance). A MOAT score of 3 is still acceptable risk for an investor. Evergreen Park has 72 years of lease left. With this amount of lease, it is enough for roughly four to five business cycles before the lease reaches its halfway point. Assuming each investor holds for an average of 7 years, there is still room for two other investors to exit the property before a potential long-term ownstay owner comes into the picture.

From a logical standpoint, the low lease issue is best mitigated by being able to exit with relative ease (Volume Effect), entry at a good price point (Value Effect), and Rental Demand to give ample rental yield for the investment if you are not using it for ownstay. For properties with a low score on Bala’s curve, you would need to pay extra attention to these factors unless you intend to stay in that property for life.

Some investors typically pay too much attention to rental yield and the rental demand of the property. For example, The Crest presents a high score on rental demand, but has a relatively moderate balance of other factors. In this condo example, we want investors to think about why they are investing in properties. Is your goal to maximise gains? To build a property portfolio for legacy purposes? Is it for rental income?

To put out a word of caution for investors that picked “rental income”, you must remember that rental income is taxable. If you are still working, it might bump you up to the next tax band. On top of that, most rental income levels are insufficient to meet mortgage payments along with the maintenance fees of the condo. This would still result in a negative cash flow until you pay off your loan. By then, the Bala curve score would have dropped. If you do not have high performance on Volume Effect and Value Effect, it might be difficult to exit with a handsome profit.

The problem but also opportunity with property investment is that every property is unique in some sense. You would have to take trade-offs in how properties perform on the MOAT Analysis. In order to make the right decision here, you as a property investor need to know why you are investing and what MOAT Analysis features matter to you the most. Unfortunately, you can’t always have your cake and eat it in the investment world. There are often too many options and not enough money to go around.

Knowing that this investment would take up a large portion of your financial portfolio should shake you up to make a proper decision. With this gravity on the financial situation, buyers now are very savvy and have high expectations of their real estate advisors.

Closing Words

The best way to prepare yourself on the property market is to educate yourself on the “what’s” and “why’s”; the ABCs of property investing. Above all, you need to have an in-depth understanding of your own needs and limitations. If you have these at your fingertips, you will have far less roadblocks when finally going through your search process for a new home or investment property.

Investors should have high expectations of their real estate advisors. If you have spent that much time and effort in doing your own research, it only makes sense that your advisor has done threefold, fourfold, a lifetime more of property knowledge. And above that, with your personal interest at heart.

The core strength of our MOAT Analysis is the ability to give you an objective comparison between multiple properties on multiple different aspects. This multidimensional approach to analysing properties helps our experts give quick, timely, and accurate insights to help you on your journey. You may contact our experts here for a consultation on how MOAT Analysis can help you on your property journey.