The rave on cryptocurrencies and blockchain technology is no stranger to Singaporeans. Your friends, colleagues, and even family members might have already discussed it with you. Is crypto and blockchain the future or just a fad? Surely, you would have been exposed to both sides of the argument. Excited friends and colleagues (and YouTubers) sharing about the endless possibilities of blockchain technology and its applications to different industries. Crypto as “digital gold”. On the other hand, “boomer” family members might have cautioned you not to go all-in on something that is not a physical, tangible asset.

The discussion on blockchain is endless. But what about something in-between? When we consider the application of blockchain in the real estate industry (we are talking about physical real estate here, not the metaverse), physical tangible assets are now able to be tokenised and transacted. Is this the future of real estate?

Inflation is the story of the year. But this is not surprising to people living in Singapore. The price of homes has been rising astronomically over the past few decades. Even with public housing and cooling measures, many would still have to cough up their coffers to buy a property. With prices continuously rising, would tokenised real estate be a sustainable way for the everyday person to participate in the investment of Singaporean real estate?

In this article, we discuss the possibilities blockchain technology can bring to the real estate market in Singapore. We are not providing any investment advice or product recommendations. This is an opinion piece where we explore the value-add potential of tokenisation and the challenges it faces before it can become a new normal in the future.

The Difference between Fractionalisation and Tokenisation

Before going any further in the discussion, there are two key terms that we need to clarify. Fractionalisation and Tokenisation. One involves using blockchain technology and the other doesn’t. Fractionalisation is a process where an asset is divided into multiple parts (usually shares, units, parts). For instance, some stock brokerage companies offer shares to be traded in the form of fractional shares, down to a few decimal places. This process basically makes expensive assets more affordable by splitting them into bite-sized chunks.

Let’s take Google shares as an example. Alphabet Inc (GOOG) Class C shares on Nasdaq are trading around USD$2,250 as at the time of writing. This price tag of S$3,123 for a share might put off many members of the public as it is simply viewed as too expensive. It is common for people to dollar-cost average and invest a constant, specific amount of money into the stock market each month. If fractional shares do not exist, it would be very difficult for people to afford to invest and buy the exact amount they want.

The fractionalisation of shares is not done by the company that issued the shares. While companies may choose to do stock splits to make their share price look more affordable, it is not the same as fractional shares. It is the brokerage companies that act as a platform that allows members of the public to buy fractional shares. This platform is crucial to be able to provide the fractionalisation service to customers. Thus, brokerage companies do value-add in this way as one example.

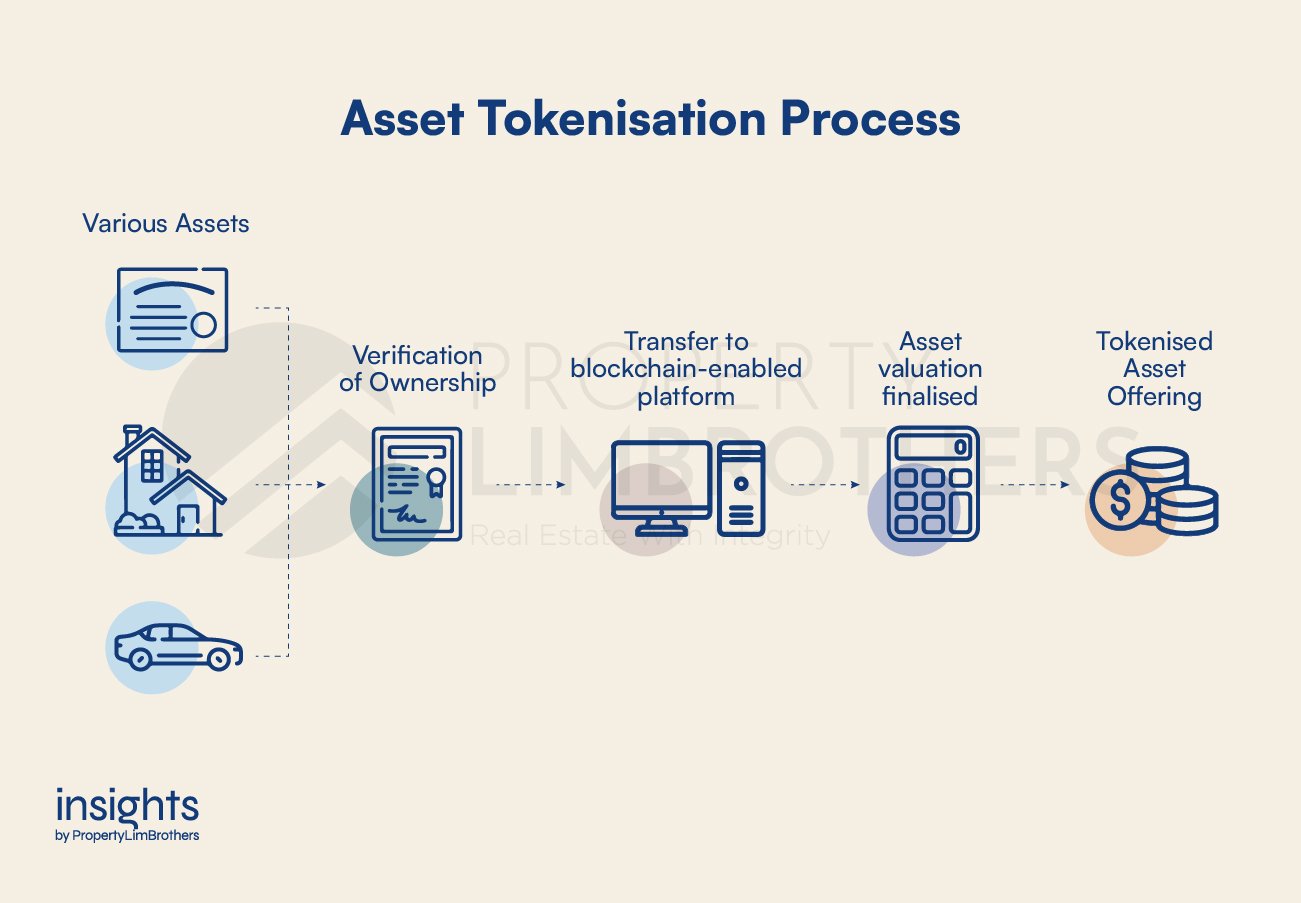

On the other hand, tokenisation is similar but the process is rather different. “Tokens are digital assets defined by a project or smart contract and built on a specific blockchain”. This is the definition given by Boston University. Tokens are different from Coins (the conventional crypto currency like BitCoin). You can refer to the link above for a detailed explanation. MAS has also put out a quick summary on blockchain technology on their website.

One big concern commonly put out (even by Bill Gates) is that digital assets, especially crypto, follow the Greater Fool Theory. This basically means that its value is almost entirely socially determined. How much it is worth is how much the greater fool is willing to pay for it. (They refer to buyers as fools because the goods are actually worth ambiguously, nothing). While this is not a very nice term to call buyers, the bottom line is that some digital assets like crypto currencies are speculative. Tokens, however, are different because they (at least in the real estate context) embody the smart contracts that are tied to physical real estate.

Taking tokens into the real estate world, the blockchain acts as the platform to fractionalise the physical real estate. Smart contracts are used to define the tokens as holding or entitled to part of the physical real estate. In other words, whoever owns the token owns part of the real estate. In some sense, each token acts as a “share” or “unit”. The token issuer here is thus responsible for both providing the fractionalised asset and issuing it to buyers.

How does Tokenisation Value-Add?

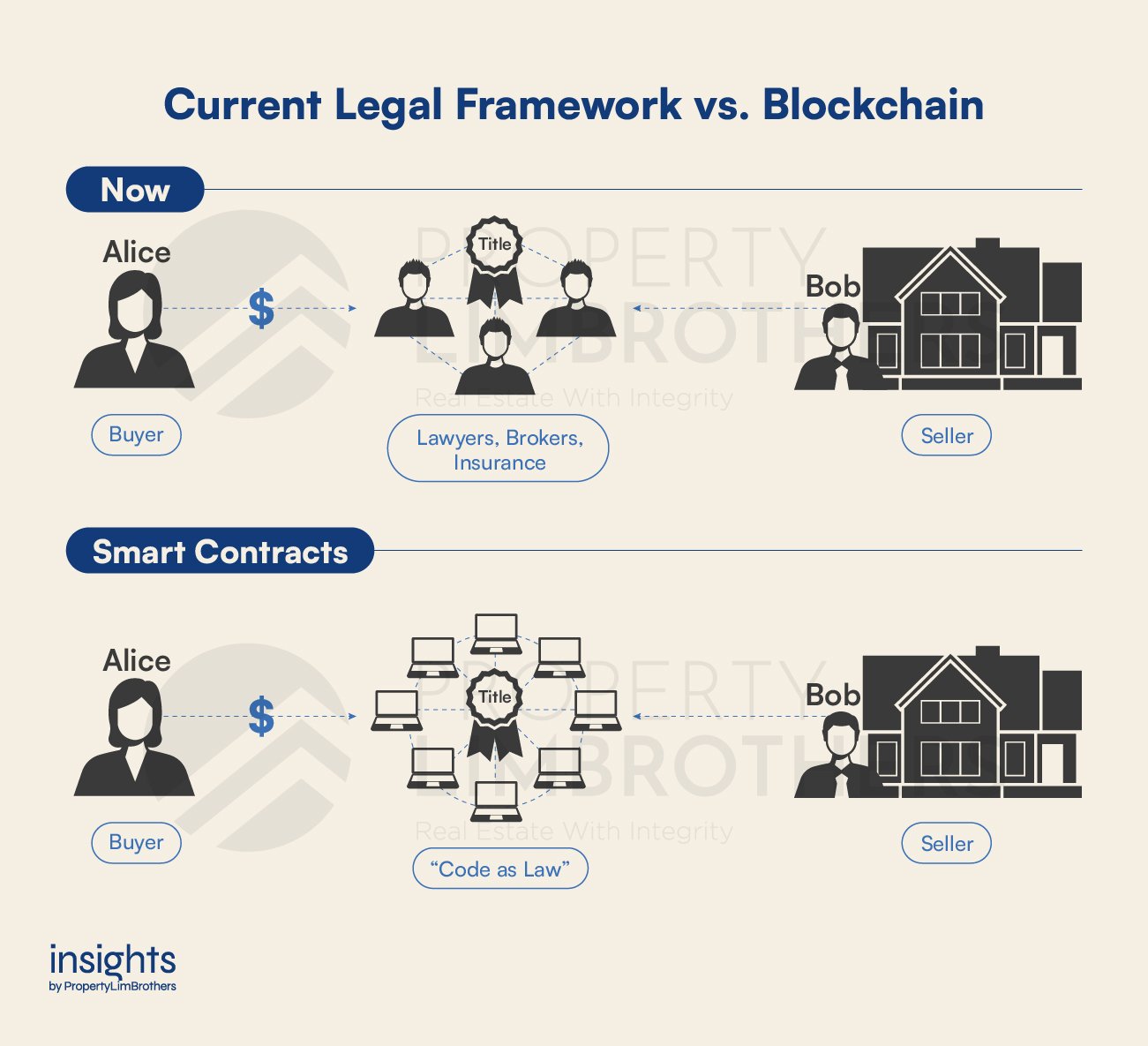

The main value-add behind the tokenisation process is the ability to go ahead with the transaction without a trusted third party. MAS terms this as a “trustless” system. This is enabled by the securitised smart contracts and use of blockchain as a platform for fractionalisation. Having smart contracts removes the need for a third party because of its self-executing function. Whenever the terms of the contract are met, it will execute the agreed-upon outcome without the need of a third party.

This is generally the main explanation behind Decentralised Finance (DeFi). The question we must ask ourselves is whether Singapore (or the world) is ready to do business without trust. A philosophical yet realistic concern. DeFi does not hold its appeal to everyone. To some, perhaps more traditional folks, trust is a necessary component of business. You want to know who you are dealing with, and that they can be held accountable for their actions. The lack of a trusted third party in transactions may not be appealing to these people.

Nonetheless, this innovation has been starting to gain traction. Investment companies such as Fraxtor offer real estate tokens, albeit to accredited investors only. MAS understands the risks presented by smart contracts and DeFi, thus limiting the demographic that can participate in investment using this form of technology. As of the time of writing, the general public would not be able to participate in tokenised real estate investments. However, fractional ownership of real estate in the form of REITs is conventional even though it mostly covers the commercial side of real estate.

Tokenisation is not an absolute necessity to fractional ownership. However, it is a step towards self-executing smart contracts. Taking this a step further, how much can a smart contract actually self-execute? While the transfer to digital assets may be made a lot simpler, it may be complicated by the existence of physical assets such as real estate. In some sense, a token is similar to a “share”. Tokens symbolise the ownership of the asset on paper. In actual reality, the management of the asset might be out of your hands. And on this management aspect, even if contracts self-execute, someone must be on the ground in physical reality to make sure that things get done.

Blockchain is definitely a useful innovation. It can be a huge boon if applied correctly in the industry. However, sometimes it might come off as just a novelty that goes with trends and buzzwords. How do we know if it is really something that value-adds to the industry? That is a crucial question that investors would have to ask.

Regulatory Uncertainty & Legal Constraints

Blockchain is slow on the take up in terms of its corporate and industry-wide application because of the regulatory uncertainty surrounding it. Because there are no firm legislation and legal frameworks surrounding this technology (apart from current MAS regulations), there are serious legal constraints that prevent the mainstream from adopting this technology.

Right now, only accredited investors can partake in tokenised real estate investments. Barring any huge scandals from happening, as well as the crypto world from collapsing, Singapore will need some time to ease this new offering to the public. There is insufficient legal precedents in the field of smart contract breaches. People are simply not sure how things will pan out if things go wrong. Smart contracts are not exactly exempt from Singapore’s contract law system. But the enforceability of these contracts are still in question.

Without market regulators and trusted third parties, code is law. The computer code behind the smart contract is basically the law and “binding” agreement between the parties involved. Some smart contracts are written purely in code while others are in English. Depending on how smart contracts are arranged and written, the outcomes in the transaction may or may not go the way you expect. All parties need to make sure that the code in the smart contract truly reflects the terms of the agreement.

Just because it is new does not mean it is bad. Blockchain simply needs more time to prove itself to the general public and earn their trust. The technology itself is not that new per se but its applications to public-facing industries and products are only starting to sprout. Apart from the regulatory uncertainty and legal constraints, the tokenisation of real estate needs time more than anything else.

From an investment perspective, the tokenisation of real estate does have its benefits. It makes it more affordable and attractive for members of the public. But we do have to remember that for residential real estate, the government’s goal is still to keep it affordable for the masses. Investors should not crowd out residents who need a place to live. In this resident-first mentality, the tokenisation of real estate might have a reduced impact if at all.

Closing Thoughts

The tokenisation of real estate is an exciting idea. Being able to say you own a digital token that represents some part of a property is thrilling to some, perhaps more hip investors. This is not really a foreign or new concept though. The fractionalisation of real estate in the form of REITs or shares of real estate companies in some sense is similar to owning a bite-sized piece of property.

While this new thrust is meaningful and value-adds to the industry in some way, there are still many challenges ahead before it enters the mainstream. Only a privileged few can dabble in tokenised real estate at the moment. Time will tell whether this is the future or just a fad.

Beyond all this talk about technology and investment, real estate is foremost a space for people to live, work, and play. Investors clamouring for returns and a piece of the pie should not crowd out the residents and more important stakeholders that are the primary users of the space. Having said this, the impact of tokenisation might be very limited. The rules surrounding its ability to tokenise residential properties would likely be stunted.

This resident-first mentality will be crucial for Singapore and its regulators to make sure that the interests and welfare of the residents are taken care of. With that, housing would remain affordable to the masses and would be free from exploitation from a minority of wealthy investors.