The parliamentary session earlier in March stirred up plenty of questions, debates, and opinions on whether the age criteria for single Singaporeans to buy HDBs should be lowered. Every one might have their own stance on this matter and we are not here to set the record straight. This article runs a simple thought experiment on what might potentially happen if the eligibility criteria for age is indeed lowered.

Here is an oversimplified summary of both sides of the debate. The proposition (WP) suggests that lowering the age criteria will help single Singaporeans meet their aspirations of home ownership and aid in their financial growth by being able to participate in the real estate market. The opposition (PAP) counters that point with the argument that land scarcity should lead to a priority-based system which allocates these scarce resources to the demographics that need it the most. We use debate terminology to label who is for or against the idea. Clearly, each side takes a different stance.

Regardless of whose side you are on, I think it is safe to say that both sides are wondering what would happen if such a policy was really put into place.

#1 How much more demand will there really be?

Everyone knows that demand for public housing will increase when the age limit is lowered. But how much more demand are we talking about? Let us think through this together. This policy will reduce the age criteria to buy BTOs and Resale flats from 35 years old to 28 years old.

Assuming that this policy is not broken into parts or implemented gradually, we will have 7 cohorts of Singaporeans eligible to buy HDB once the policy is in place. This will create an initial demand shock of 7 cohorts, subsequently only 1 additional cohort will be eligible to buy HDB in the next year (those 27 turning 28). Dealing with this initial demand shock will be an important policy consideration should the debate get serious on this matter. One way might be to gradually reduce the age limit, 1 year at a time to see the effects of the demand shock on price before implementing any further changes.

Image courtesy iStock

Another important caveat is that the actual demand shock isn’t the entire cohort. The demand that will be opened up will only be people aged 28-34 who are single, willing, and able to purchase a BTO or Resale flat. According to the population brief by the government, the estimated population size for 30-34 is approximately 250,000 (both males and females) and 25-29 is approximately comparable. That means that each cohort is around 50,000 people.

Let’s then look at the percentage of people who are single. From singstat, the latest data from 2021 shows that 31.3% of residents aged 15 and over are single by marital status. Assuming that this number is also the average across cohorts, each cohort should have 15,650 singles. How many of these singles are able, and more importantly, want to buy a HDB of their own? Some who are “single” by legal definition might be in a relationship. Others might simply prefer to stay with their parents. And more might just rent rather than make such a long-term commitment to buying a property. Our conservative ballpark estimate for the singles who would be willing and able to buy a HDB would be 5,000 individuals per cohort.

#2 How will this impact BTO and the Resale HDB market?

Given the current state of the property market, it is unlikely that the government will implement a policy unlocking 7 cohorts of demand all at once. It will likely be opened up year by year. If we follow this assumption, we will see demand increase by 10% more than usual in the first year and steadily reduce to 6.25% increase in the seventh year. Even though this is a gradual increase, the aggregate demand would increase by approximately 70%. This is a huge number, with simple guesstimates of course.

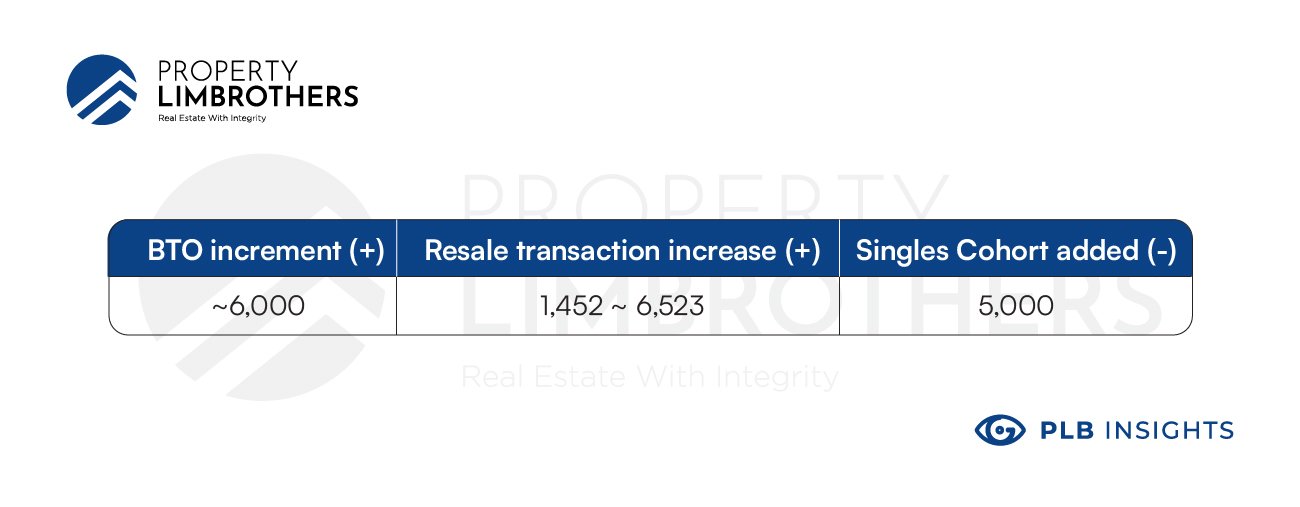

HDB plans to increase the number of BTO flats supplied to 23,000 per year in 2022 and 2023. This represents only a 35% increase. For Resale HDBs, we use the number of transactions in 2020 and 2021 to estimate the existing demand crudely. We see an increase in transaction number from 23,297 in 2020 to 29,051 in 2021. This is an extremely rough guide of 24.7% increase in cleared demand, previously the year-on-year increase in cleared demand is around 5.5%. Percentages here are not as helpful as the base numbers for BTO, Resale, and increase in demand from policy change are all different. Here is a table to look at the numbers in more detail.

We take the average BTO increment per year with the average of resale transaction increase over the past 2 years and compare it to the increase in demand from singles in each cohort. While the situation does not look that bad here, anyone can imagine how around a 10% increase in yearly demand would look like for the price situation.

It is safe to say that the government has not planned for such a policy to just be implemented overnight. The BTO increment is planned to accommodate the existing growth in demand, which is already oversubscribed. While retail transactions see a natural increase of around 1452 to 6523 transactions per year, even an addition of 2500 (half of the singles buying) is a tremendous amount of yearly increase.

Image courtesy PropertyGuru

The real question is whether or not the growth in BTOs and Resale transactions can accommodate this amount of growth each year. For BTOs new releases or Resale transactions to grow at 6-10% a year rather unheard of. It raises some serious questions on sustainability and affordability. A demand spike as much as this could end up pricing out other buyers who also need public housing.

BTOs would be even more oversubscribed despite the extra supply. In addition, Resale transactions might spike with price and inflate quite substantially. Despite these hypothetical consequences, it might not be fair to say that the proposition for this policy change is ridiculous. The current infrastructure is designed and planned for the current growth numbers. Should this be a serious policy change, it is not fair for the proposition to work with the current growth plans and planned increments. That being said, it is clear that a solution is required to cater to this additional demand (should it be implemented). We’ll let the public and parliament to deliberate and debate on this issue.

#3 Will this trickle down to other parts of the Real Estate market?

Based on this thought experiment, a plausible result would be that price and volume would increase substantially year-on-year on the guesstimated order of 6-10% more than expected. With this being the case, affordability will be an issue for lower income households. As the price of HDBs increase, we might see less room for future appreciation after MOP. The price of HDBs inching closer to condominiums would also mean that the upper band of HDB buyers would start considering condos. This might end up pushing up the price and demand for condominiums (private and EC) as well.

Image courtesy Straits Times

However, any further predictions based on predictions would just be too much of an extrapolation. After all, this is based on a thought experiment inspired by parliamentary debate and some real numbers from the ground.

Closing Thoughts

To round up our little experiment, we considered 3 main questions on the proposed lowering of the HDB age criteria:

-

How much more demand will there really be?

-

How will this impact BTO and the Resale HDB market?

-

Will this trickle down to other parts of the Real Estate market?

Of course, we use extremely rough guesstimates. Please do not take these numbers seriously. There are plenty of assumptions in arriving at the numbers that we have and they could very well be dispelled by reality.

Nonetheless, we believe that thought experiments such as these might give us a good exercise in trying to understand how events and policies might or might not impact the market with a little bit of thinking. We hope that this was a fun and eye opening exercise for you too! If you want more insight and opinions on these matters, contact us here!