Should I stay or should I go? Investors and real estate veterans ask this question over and over again, about where to allocate their investable assets. Having a property portfolio consisting of overseas properties may seem like a “sophisticated” diversification move, but are you sure that is the better investment strategy?

Depending on how you look at it, diversification may or may not be the greatest strategy for managing a portfolio. But diversification for the sake of diversification might hurt your portfolio more than it does good.

In this article, we highlight the most important questions you should ask yourself or your real estate broker before seriously considering overseas property investments. We make the case for why buying Landed properties in Singapore may be a better option than overseas properties for most people. Stay tuned to find out more.

Opportunity or Red Herring?

Let’s get real, what are the benefits of buying properties overseas? Is it a real opportunity for property investors or simply another red herring? Property ownership overseas can go from being a strategic portfolio play, a casual holiday home, to a complete flop in asset allocation. The purpose for buying properties overseas should be clearly defined even before looking at listings of properties overseas.

Perhaps, what tempts most Singaporeans is that buying Landed homes here in Singapore is way too expensive. A decent piece of Landed real estate can easily go beyond S$5M into the 8 digits. With this framing, suddenly Landed properties overseas might become a very attractive idea. Be it Malaysia, Australia, or the UK, overseas Landed properties suddenly become an opportunity for locals to own their own Landed home.

While there is nothing wrong with wanting to own a status symbol or your own piece of land, when it comes to the dollars and cents, there can be a clear difference between a good and bad decision. If you are not concerned about property valuations and gain, then attaining the goal of owning Landed properties through overseas properties might not be a bad idea.

That being said, buyers need to know not to be misled by emotions when making a purchase of this size. Long-term financial considerations for the individual buyer and the family should be in the picture as well. An opportunity for someone who wants the cheapest and fastest way to own a Landed home may be a distraction to another who wants to grow their wealth.

Therefore, buyers would need to know why they want to buy a Landed home. Does buying it overseas enhance the overall prospect for the buyer? Or does buying a Landed home locally give a better risk-reward ratio while fulfilling all the needs and wants?

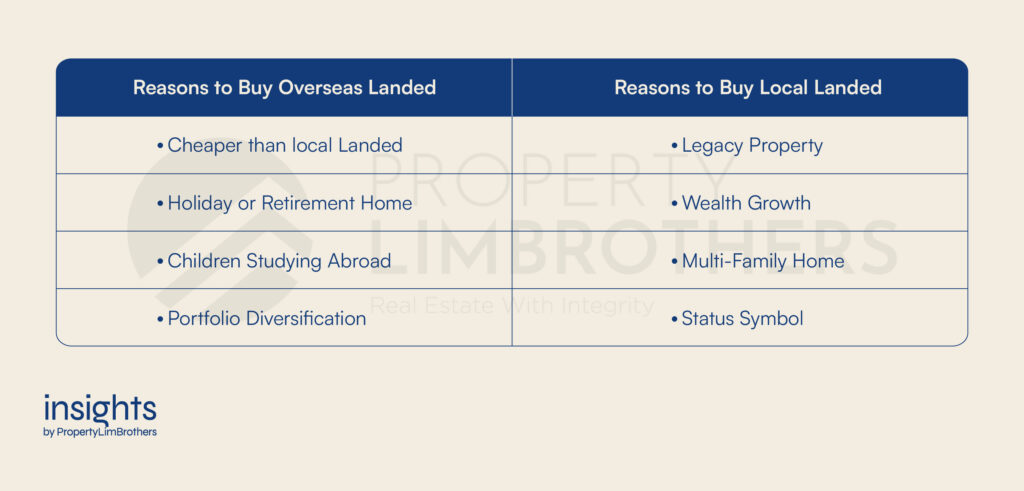

Here are some common examples of why people may or may not buy Landed property abroad. This list is not exhaustive, and there may well be many other personal reasons for the purchase.

What is it that you want from a Landed property? Can it be fulfilled through other means? Could it be fulfilled through local rather than overseas properties? There are specific purposes that overseas property can fulfil that are circumstantial and unique. Such as your favourite holiday spot that you plan to visit often in retirement. Or that your children are studying abroad and it makes more sense to buy than to rent (this depends as well).

An opportunity in the local market that you might have missed is that the landed property market in Singapore is protected to some extent from foreign interest. Singapore Land Authority (LDAU) approval is needed for foreign individuals and entities to purchase landed property in Singapore. Most of the time, only landed properties in Sentosa are granted LDAU approval.

The landed property market in Singapore is driven almost entirely by Singapore citizens. (Of course, foreigners that take up Singaporean citizenship are counted too). Even with the capped demand, the supply of landed homes is still rather limited. It is one of the few property classes that have better prospects for appreciation.

Landed properties also make a good option as a multi-family home. Using the Landed property as a stay-in property might also make more sense in Singapore than overseas unless you are looking to relocate along with your family.

Geopolitical Turbulence — What does it mean for Foreign Property Owners?

There are words circulating in the media of a “new international order”. What do the rising geopolitical tensions around the world mean for foreign ownership? Are we moving through a period where countries choose nationalistic isolation over international cooperation and prosperity?

A prolonged period of geopolitical tension is bad news for foreign property owners, regardless of your nationality and where you have bought your overseas property. Perhaps, it will matter more for some countries as opposed to others. But the bottom line is that the world now is a lot more uncertain.

In such environments, foreign property owners (or even local ones at that) might start to shrivel up. Given the poor macroeconomic conditions that follow, it would not be surprising to see more and more high-net-worth individuals (like celebrities) start to sell their property holdings and sit on cash.

Uncertainty across national boundaries is not an encouraging state to be in for foreign property owners. If this persists, we might see less foreign interest across the board in property markets. More focus on cash, and other assets that are not as exposed to geopolitical turbulence.

If there is something we can learn from where the world is headed, it is to be safer than sorry. Conservatism and prudence in where we put our money would matter a lot in the coming quarters. The volatility in political and financial matters will probably continue to increase.

Of course, for foreign property owners who currently have a portfolio of properties across the globe, this is not a recommendation to panic sell your entire portfolio. It is more of a cautionary word for prospective investors looking to dabble in overseas markets. It is simply not a very great time to be exploring without deep knowledge and experience in these markets.

Foreign property owners would need to reevaluate their property portfolio exposure to geopolitical risks. Should you start consolidating your portfolio and focus on holdings that you really think will succeed? Trimming off losers or high risk assets may be a smart intermediate move as the markets readjust and make sense of the turbulence.

As governments around the world focus on urgent domestic affairs such as food and energy security, we might see resources from urban development be reallocated. Rather than be carried away by promises of gentrification or development of surrounding areas, international real estate investors need to focus more on the here and now. Does the existing location and amenities justify the asking price?

Some newer international real estate investors might have been burned before. In the not-so-recent case of property investments made by Singaporeans in Malaysia Landed properties, be it Johor Bahru or Kuala Lumpur, promised developments in the area might not manifest. Businesses and savvy investors might not be as keen in the market as you are. The grass seems to be greener on the other side, but that is hardly the case when we are comparing Singapore as the base.

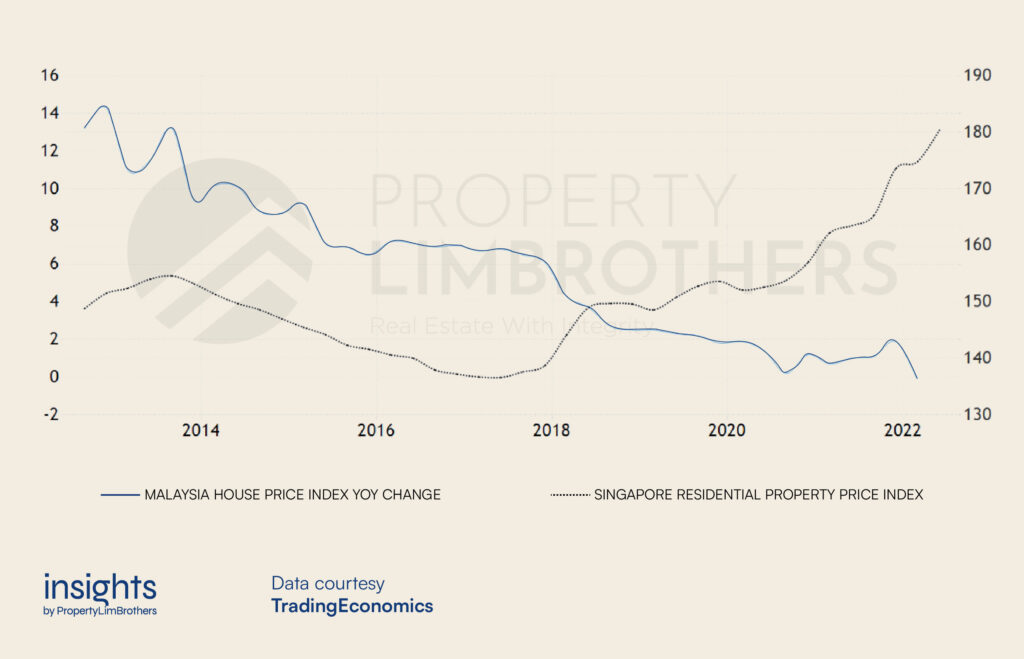

Singapore’s housing market fundamentals are solid. And few property markets can surpass the stability and value that can be found in our local markets. Comparing the housing markets in Singapore and Malaysia, growth in Malaysian markets has been decelerating as compared to Singapore’s recent acceleration in the post-pandemic world.

It might appear a little misleading so we need to clarify that Malaysia’s house price index is calculated on a year-on-year change basis. Whereas Singapore’s residential property index is based on the calculation against 2009 as the base year. Nonetheless, we can still see that the rate of change is going in opposite directions for the two markets.

In this example, buying into overseas property might dilute your returns and potentially expose you to uncertainty in foreign markets and their respective policy decisions. On top of this, foreign buyers should always be aware of the stamp duty situation for different countries.

This could drastically affect your decision, especially if the landed properties you’re looking for don’t come cheap. Perhaps you may not even be allowed to own landed properties there at all! It is best to do your due diligence to make sure that the market is friendly for foreign buyers.

Are the Additional Risks Justified?

Overseas properties are touted for their diversification purpose in property portfolios. But do the numbers add up? Overseas properties incur more risk than most people are willing to admit. The key benefit of diversification is to reduce the reliance on a single asset class or category in general.

In the ideal situation, diversification helps you hedge your risks and gives you a better risk-reward ratio. Let’s say all your assets are in Singapore. Your cash, stock, bonds, job, home; everything is in Singapore. If disaster hits (touch wood), all your assets will be affected. That is because underlying all those assets have one thing in common – they are all located in Singapore.

As a result, if anything happens to Singapore (good or bad), most of the assets will be correlated and move in the same direction. At least in theory. Thus, one of the ways to diversify is to go into assets which are uncorrelated to the ones you currently have. Your returns may or may not get better.

Typically, this is done by diversifying across asset classes, industries and/or countries. It works by lowering asset-specific or country specific risk. Through diversification, reliance on a single type of asset, industry or country to perform is reduced. Though, this is not entirely without tradeoffs.

In the case of buying Landed property overseas rather than locally, you reduce the country specific risk of being exposed to Singapore (people need to ask if this is necessarily a bad thing). The tradeoffs would be that your overseas Landed property will be exposed to Foreign Currency Risk, Foreign Policy Risk (the policy of the country you’re buying in), depending on the country you might also experience an increased risk of Natural Disasters, Climate Change, their country’s economic health, etc.

If these additional risks are not enough to turn you away from the decision, it should at least give you a broader sense of what you need to be aware of. You need to be very selective about your choice of overseas Landed properties. And be savvy on the actual prospects of the property’s ability to appreciate in the future.

In many other countries around the world (Europe, Asia, Americas), land scarcity is not as big an issue as it is in Singapore. The fundamentals of other real estate markets might be driven by many other factors. And you should know what those are before diving in to purchase.

Pragmatic Caretaking — Who will manage the Property Holdings?

This is ultimately the most pragmatic question on the logistics of owning an overseas property. It is also an important matter of trust. Do you plan to rent out the property to beef up the returns? Or do you intend to just hold it for your own stay even if you’re not in town? More importantly, do you have a realtor that you can trust from that country?

Purchasing properties overseas is a complicated process. Especially if you do not have a personal network that you can rely on to help you better understand the market and manage your property holdings. Having friends or family in that other country (or even having stayed there yourself for a period of time) can help assuage some concerns through the familiarity from experience.

Regardless, the issue of managing properties overseas alongside the administrative issues can be easily underestimated. Everything might look good on paper, until you get missed mails, runaway tenants, or burglaries on the table. The geographical distance from your overseas properties might be more trouble than it’s worth in scenarios where you’re new to the game.

Beyond the logistical issues of how the Landed property will be maintained and taken care of, you should ask yourself if you have the time and attention to monitor your overseas holdings. Compared to other assets, managing overseas property might not be as “passive” as it sounds.

Conclusions

The better investment strategy is the one that gets you to your destination faster. Returns are not always the indicator of “better” for the individual. It depends on why you’re actually thinking of buying overseas properties in the first place.

For those of us with the dreams of owning a Landed property one day, perhaps taking the “shortcut” and owning one overseas might be more trouble than it’s worth. Unless you have plans of relocating, or have family members planning to stay overseas, it might make little sense to dabble in such uncertain markets.

Here are some questions you ought to ask yourself if you are considering investing in overseas Landed properties.

- What is the purpose of your overseas Landed purchase?

- Can this need be met through other means (diversifying through other asset classes)?

- Are the fundamentals of the foreign property market strong?

- What are the factors that drive return in that market?

- Are there any hidden risks of your overseas Landed property investment?

- Who and how will the property be managed in reality?

If you have your own set of questions and are still unsure as to which strategy is better for you, feel free to reach out to our experts on the matter. We are more than happy to learn more about your personal situation and give you a second opinion on whether the decisions you are making fit your best interests. Until then, thank you for reading and supporting PLB Insights!