COVID-19 has been an ongoing, extensive problem with an insidious reach in terms of its effects on society. Likewise, it has impacted the Singaporean real estate market as it has in other countries.

A changing office real estate landscape and a general consensus of wanting more space in their property have driven homebuyers to shift attention from the central to city fringe homes.

Hopefully, COVID-19 will not be here for much longer, but we have to admit that its effects are deep-rooted into our society, so what does this mean for us as homebuyers?

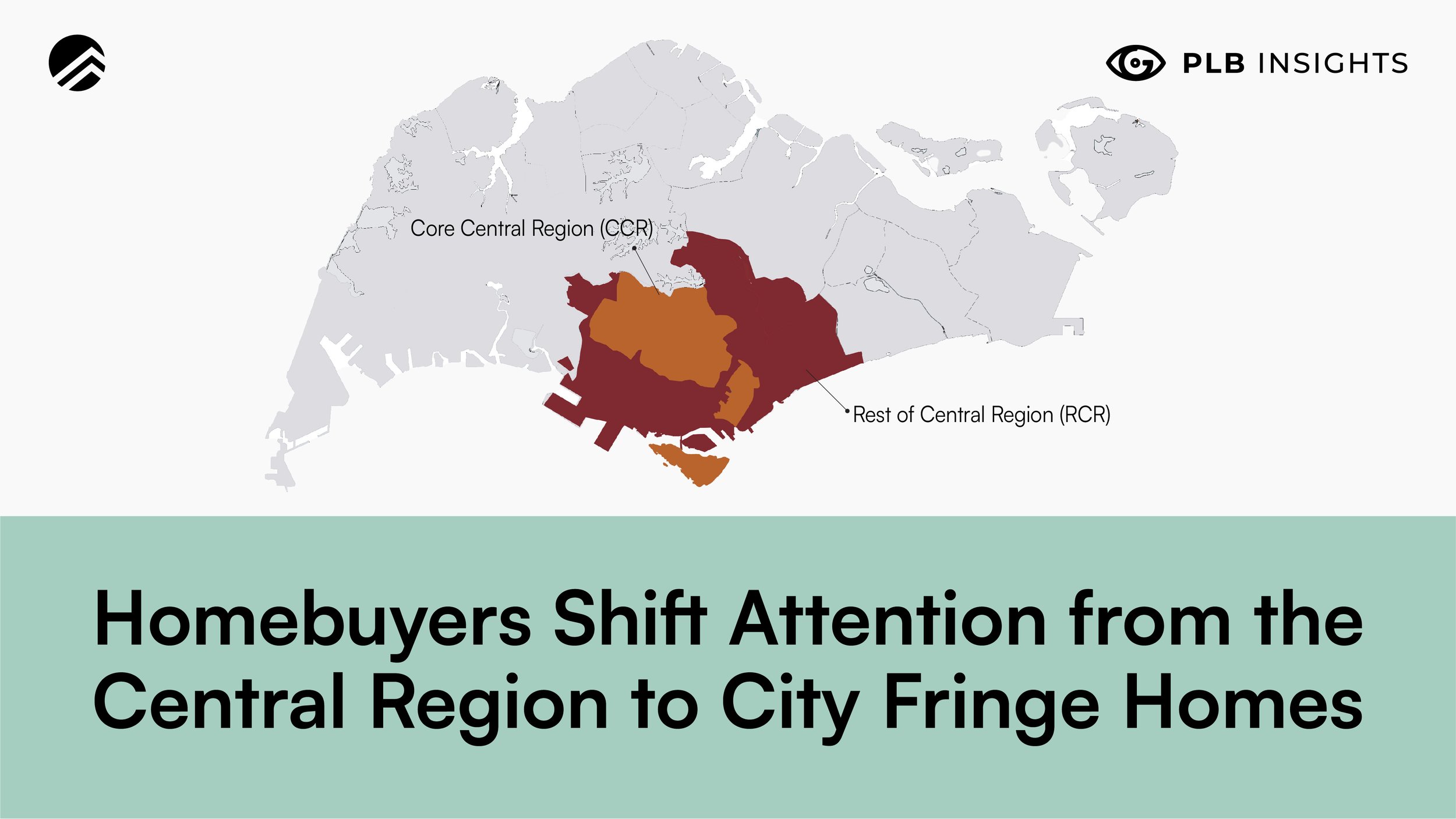

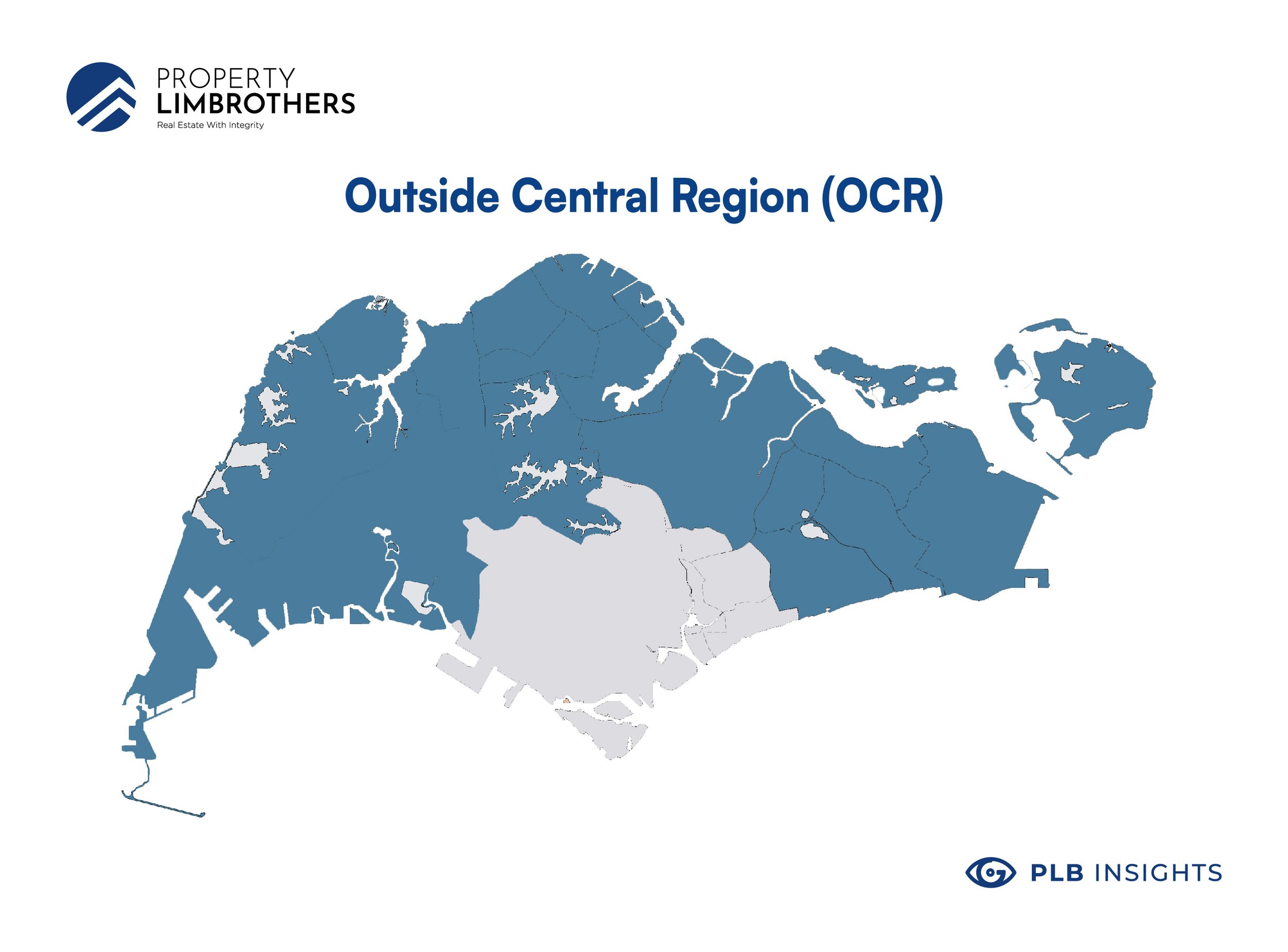

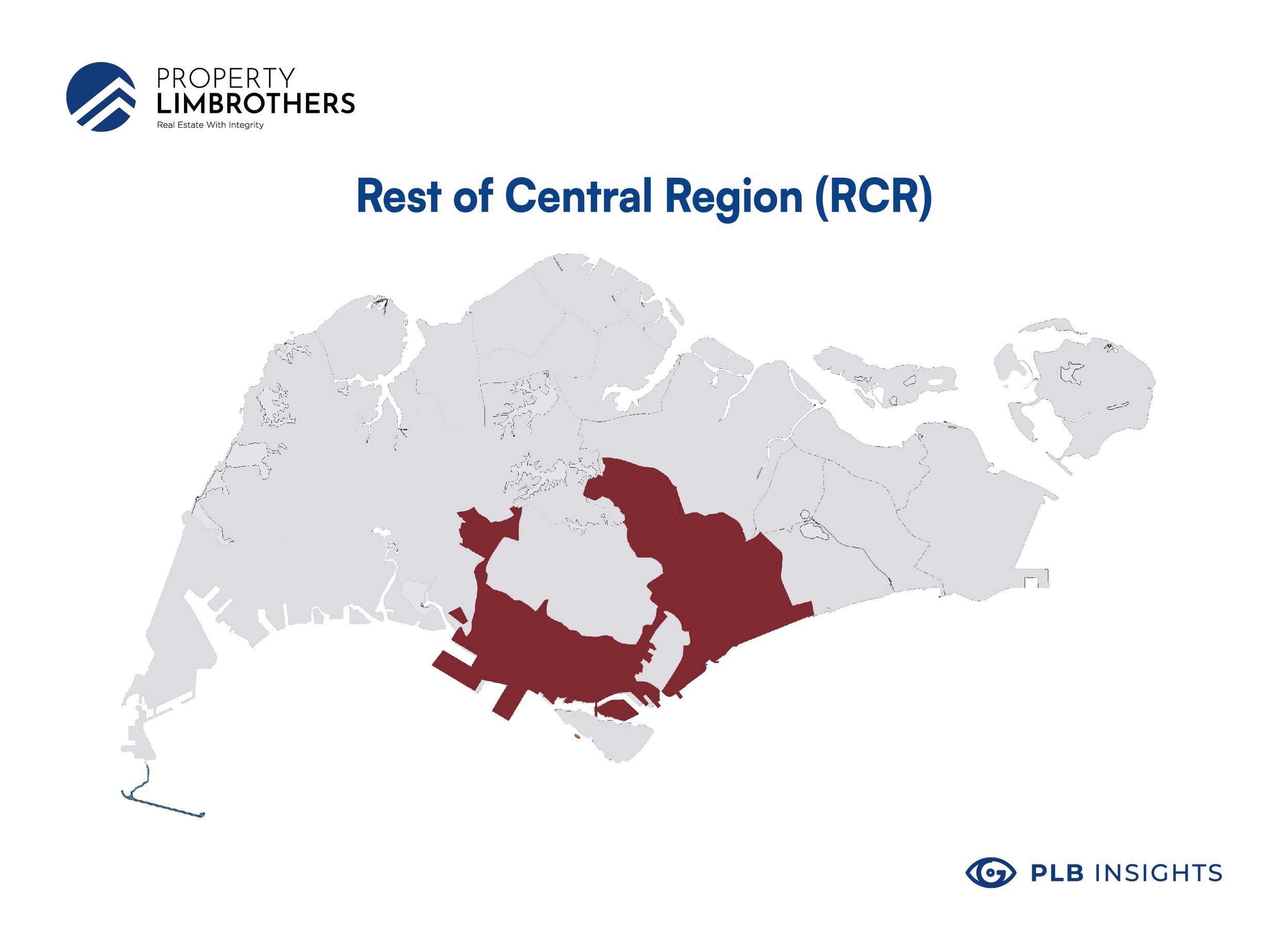

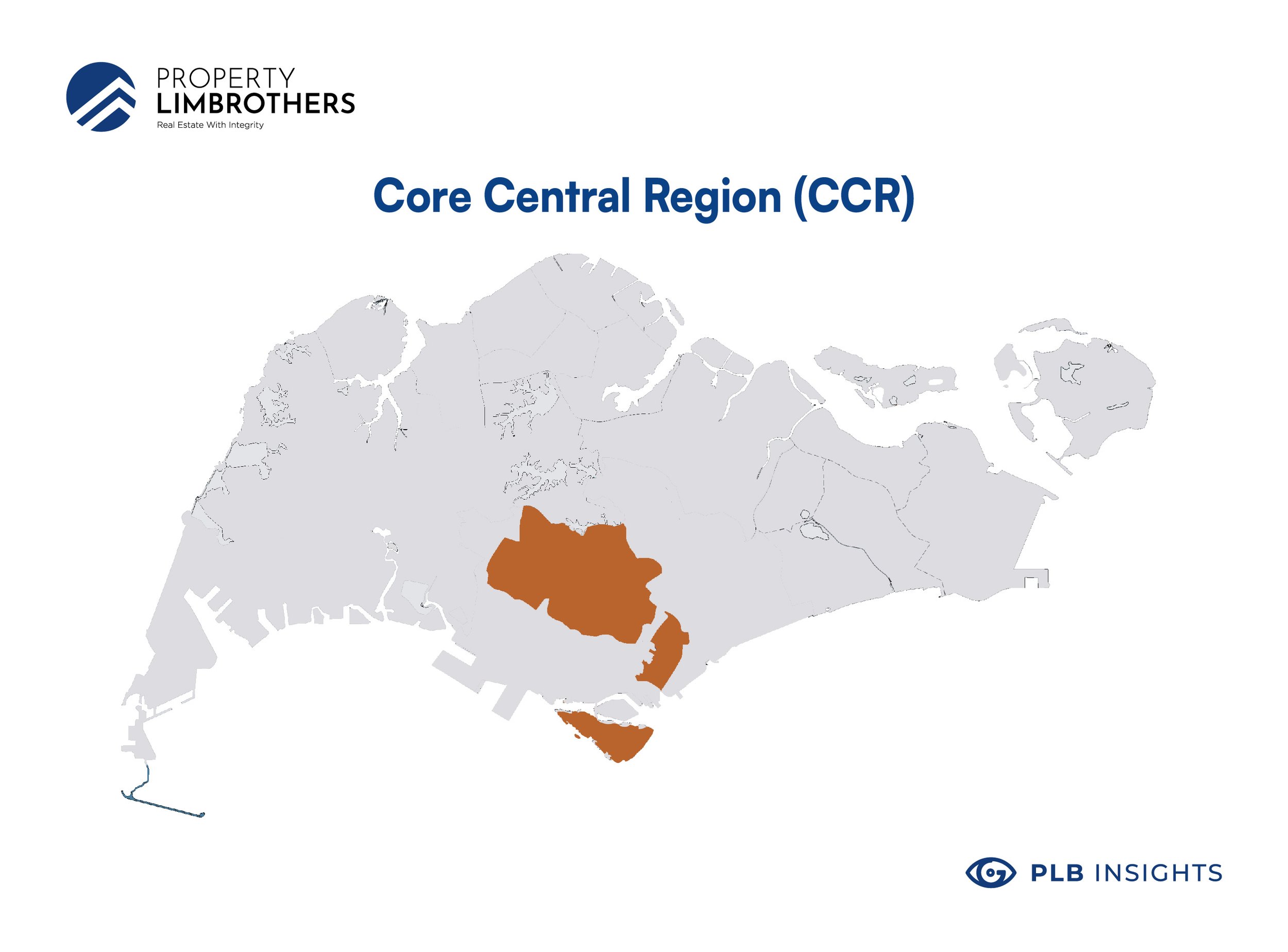

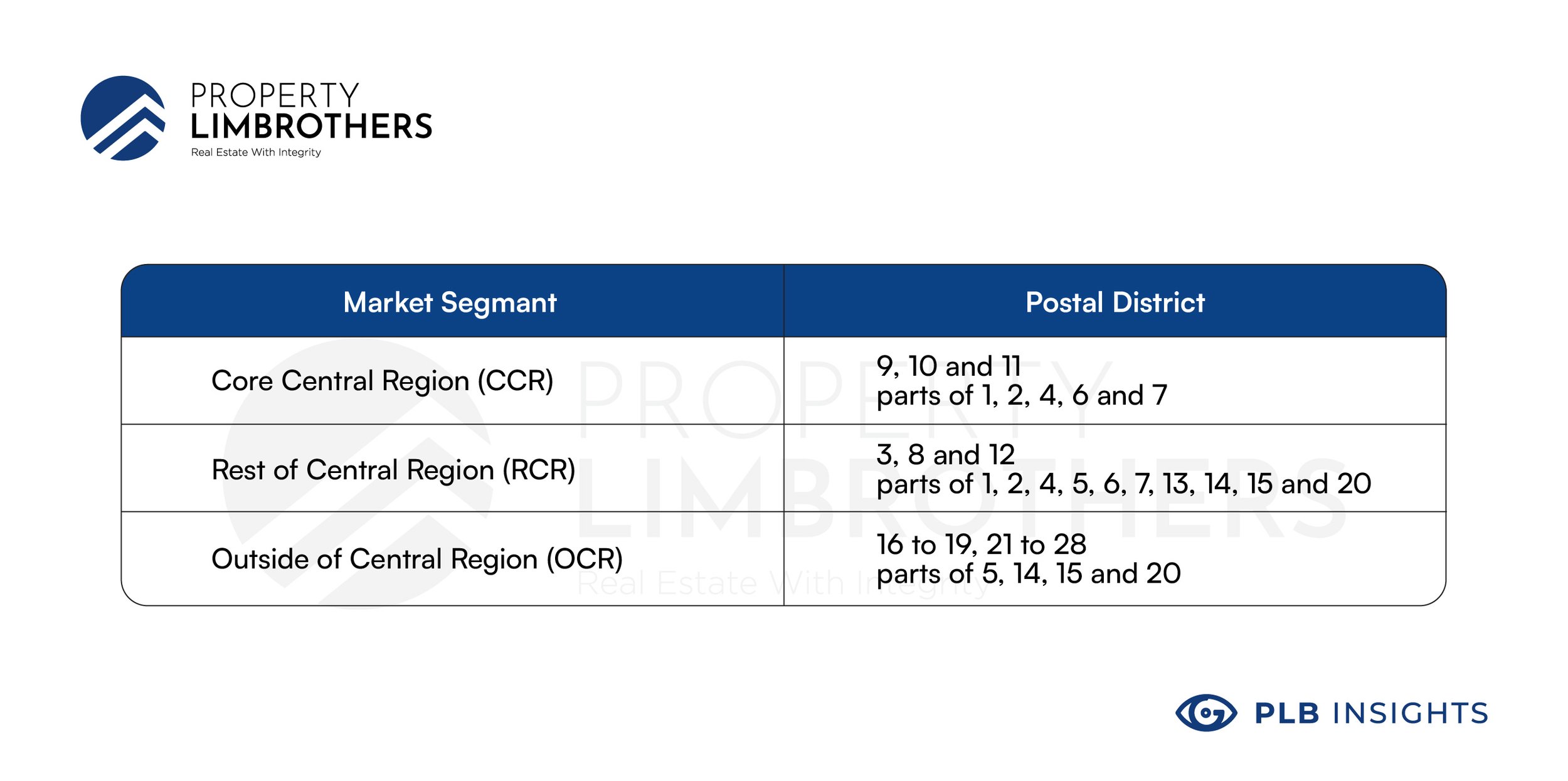

CCR vs RCR vs OCR

The Urban Redevelopment Authority (URA) has divided Singapore into three “Market Segments”, namely — the Core Central Region (CCR), the Rest of Central Region (RCR) and the Outside Central Region (OCR) encompassing all 28 of Singapore districts.

Outside Central Region (OCR)

Rest of Central Region (RCR)

Core Central Region (CRC)

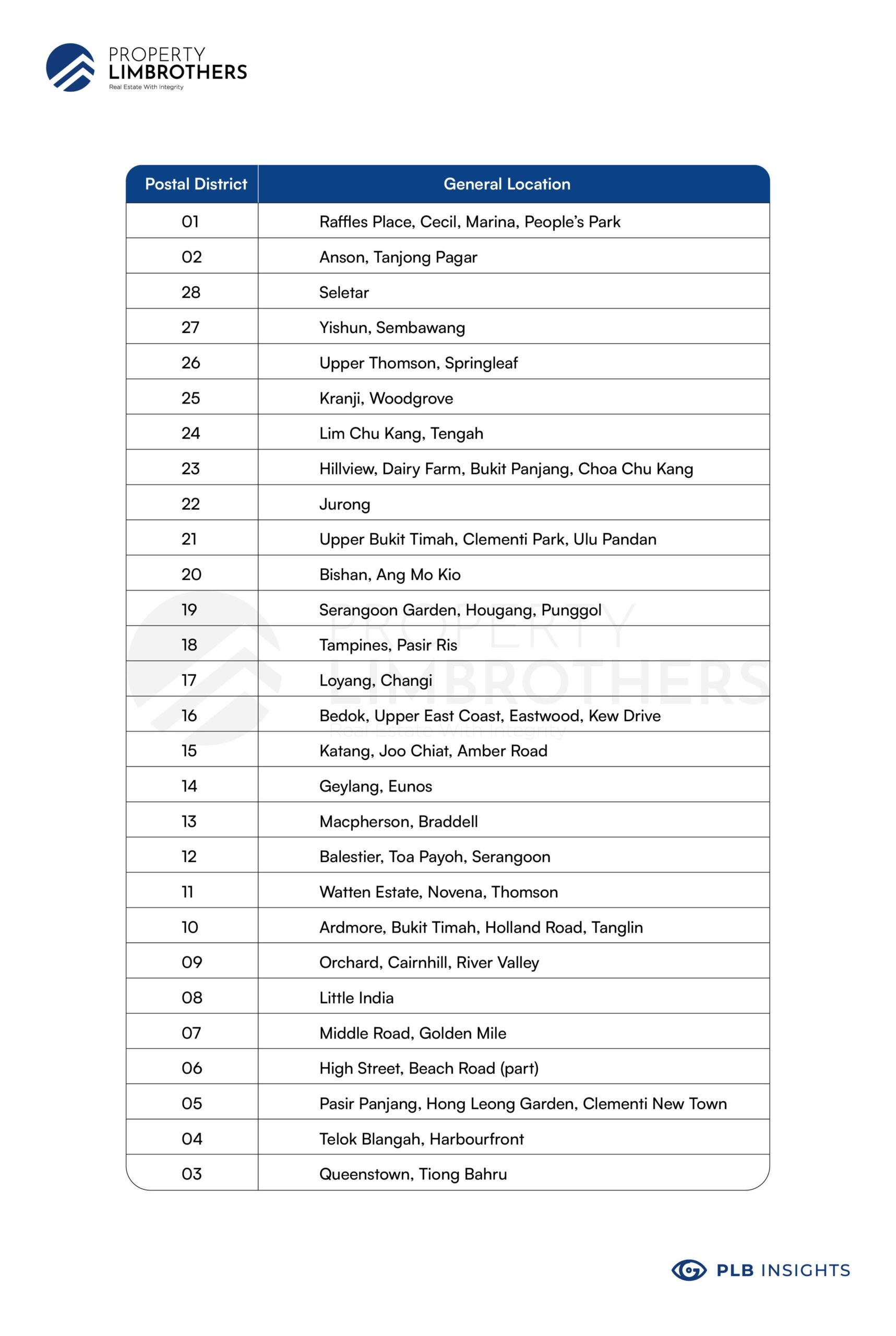

Listed below are the postal districts and the general location in reference to the towns which we are more familiar with:

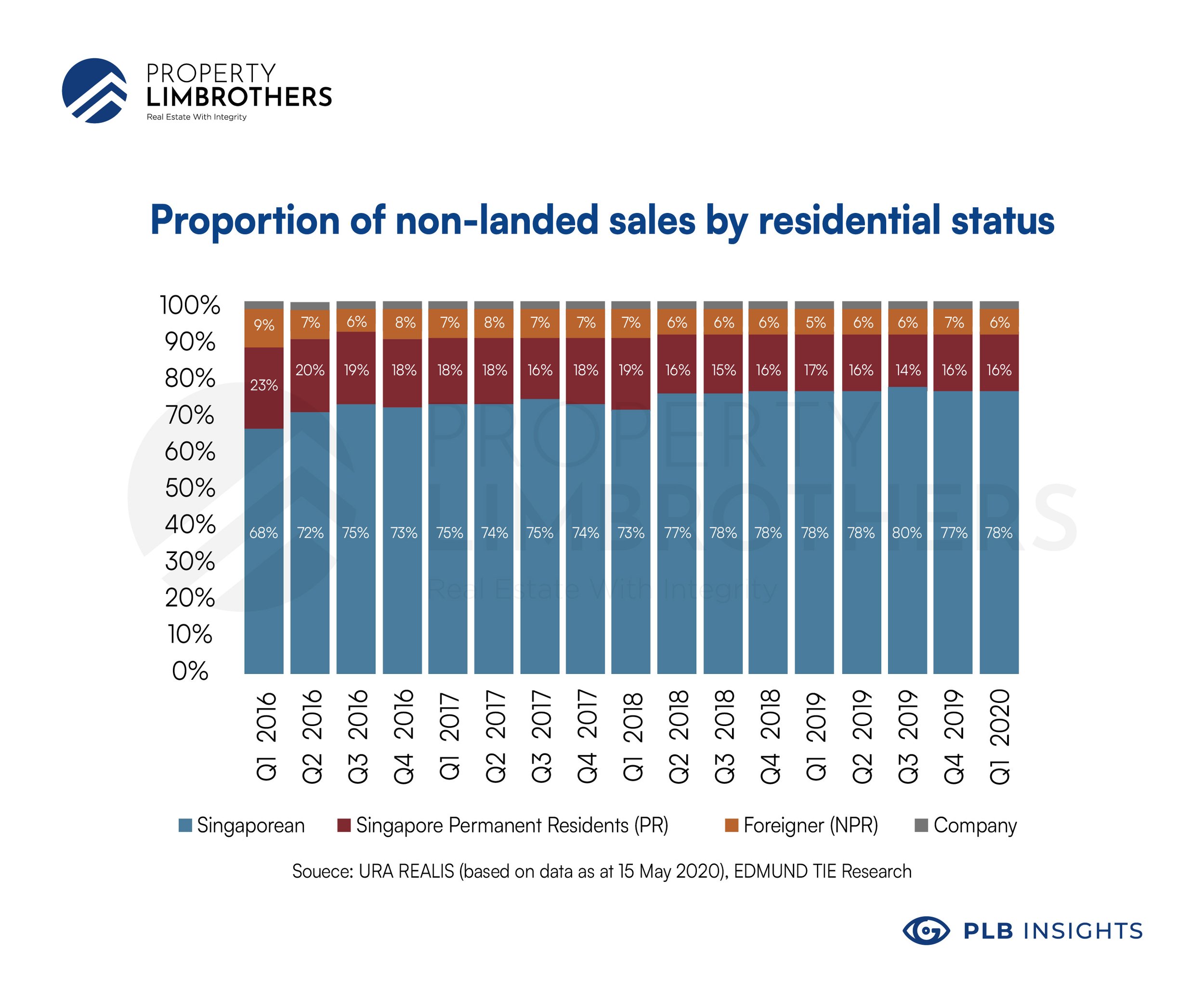

Decreasing demand for Core Central Region (CCR)

CCR segment used to be supported by Foreign Buyers

In the past, the CCR audience was primarily made of foreign investor-buyers as they had a stronger preference towards purchasing the premium address. With our wealth, income, and estate taxes considered lower as compared to international standards.

Furthermore, Real Estate Capital gains are not taxed in Singapore, thus attracting foreign investor-buyers to invest in the Singaporean Real Estate market in the form of a physical property to hedge against inflation through capital appreciation.

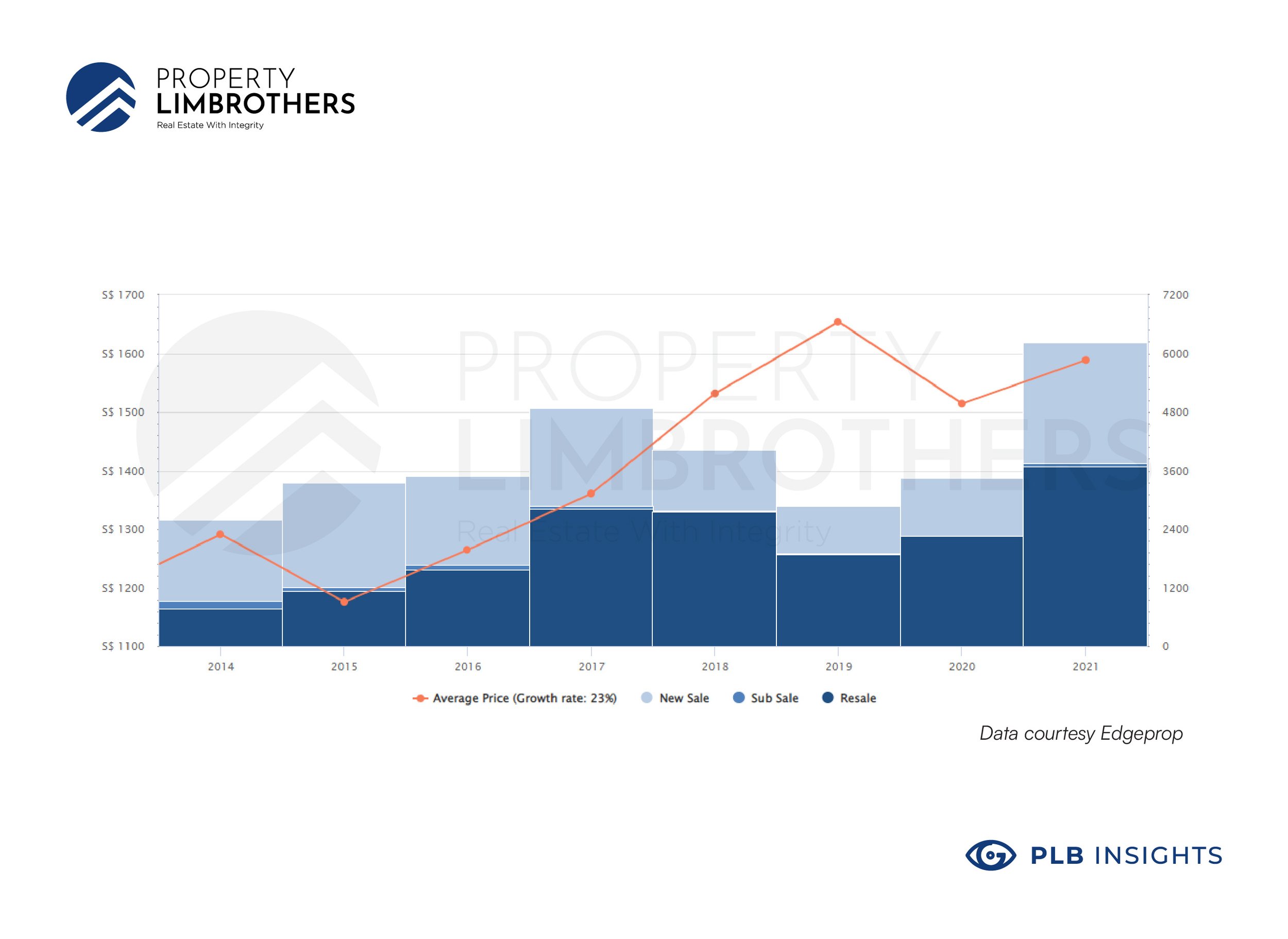

The historical statistics above show that the proportion of non-landed sales by residential sales bordered around 20-23% in FY2016. However it has since dropped over the years to 16% in Q1 of 2020.

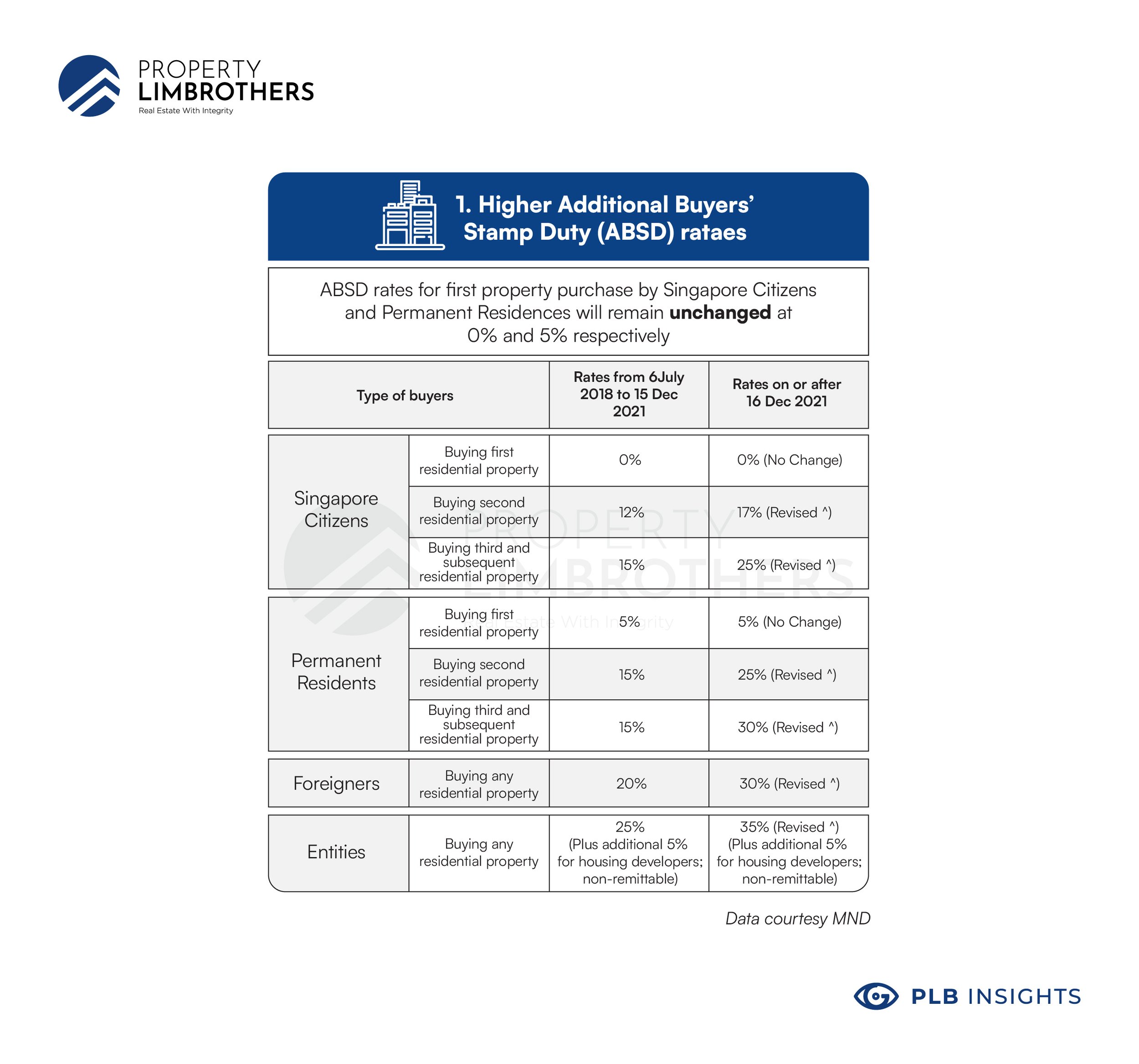

We hypothesise that the multiple rounds of cooling measures that Singapore has experienced have had a deflationary effect on foreign investor-buyers on CCR properties due to the increased cost of purchase.

Additional Buyer’s Stamp Duty was first introduced on 7 December 2011 and has undergone four iterations, with the latest round of ABSD rate revision on 16 Dec 2021.

We foresee that the recent round of cooling measures will only strengthen the trend in attention shift from central to city fringe homes and reduce the number of foreigners transacting in Singapore’s real estate market.

However, we would not be able to accurately predict if there will be a resurgence in transaction volume by foreigners, as real estate remains as one of the more favourable forms of investment and store of capital, this progression would largely be dependent on the macro outlook for foreigners in the region and internationally.

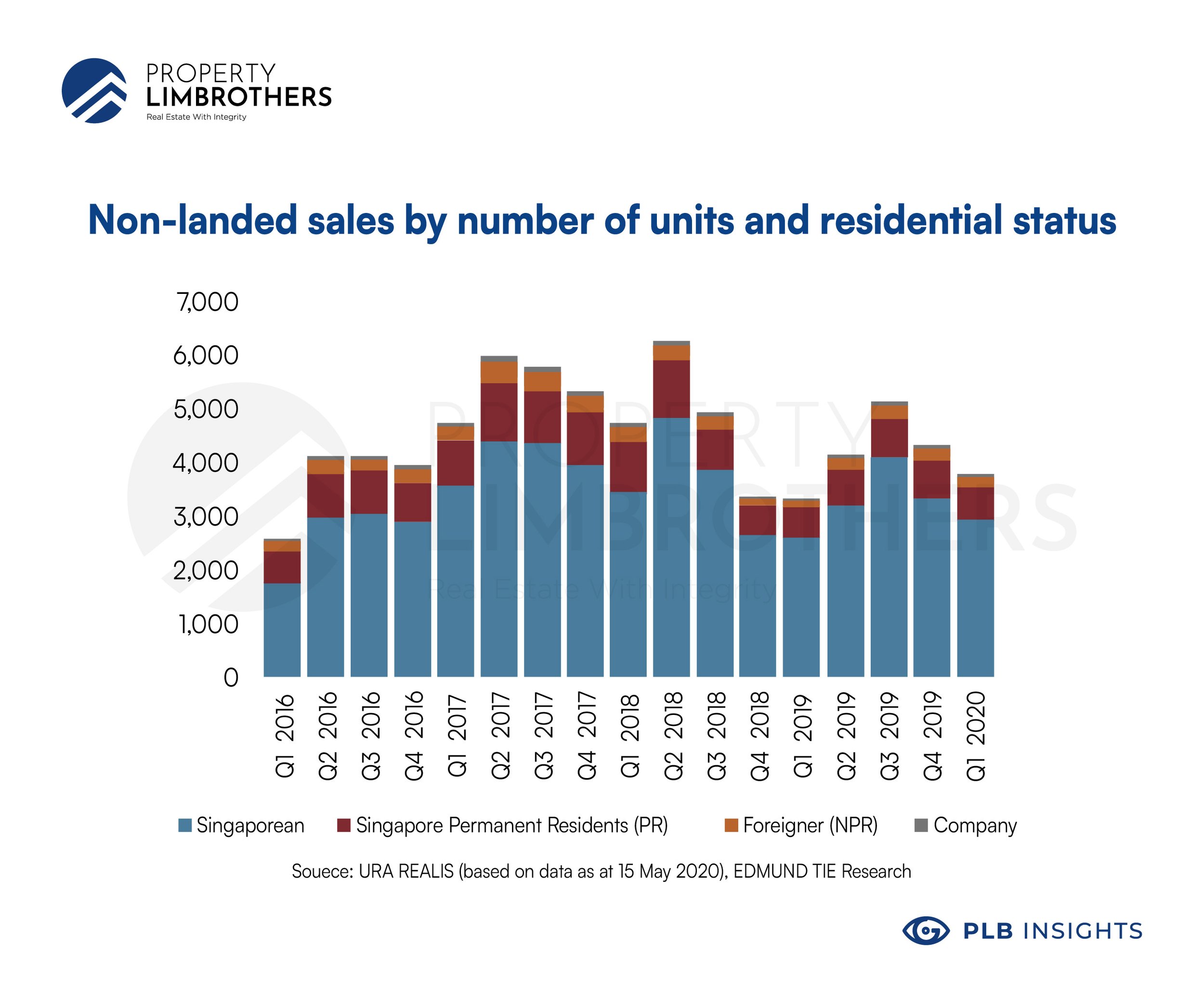

Overall volume and demand has dropped. The current market is currently self-supported by locals, with more than 80-90% locals making up for total transactions in the real estate scene.

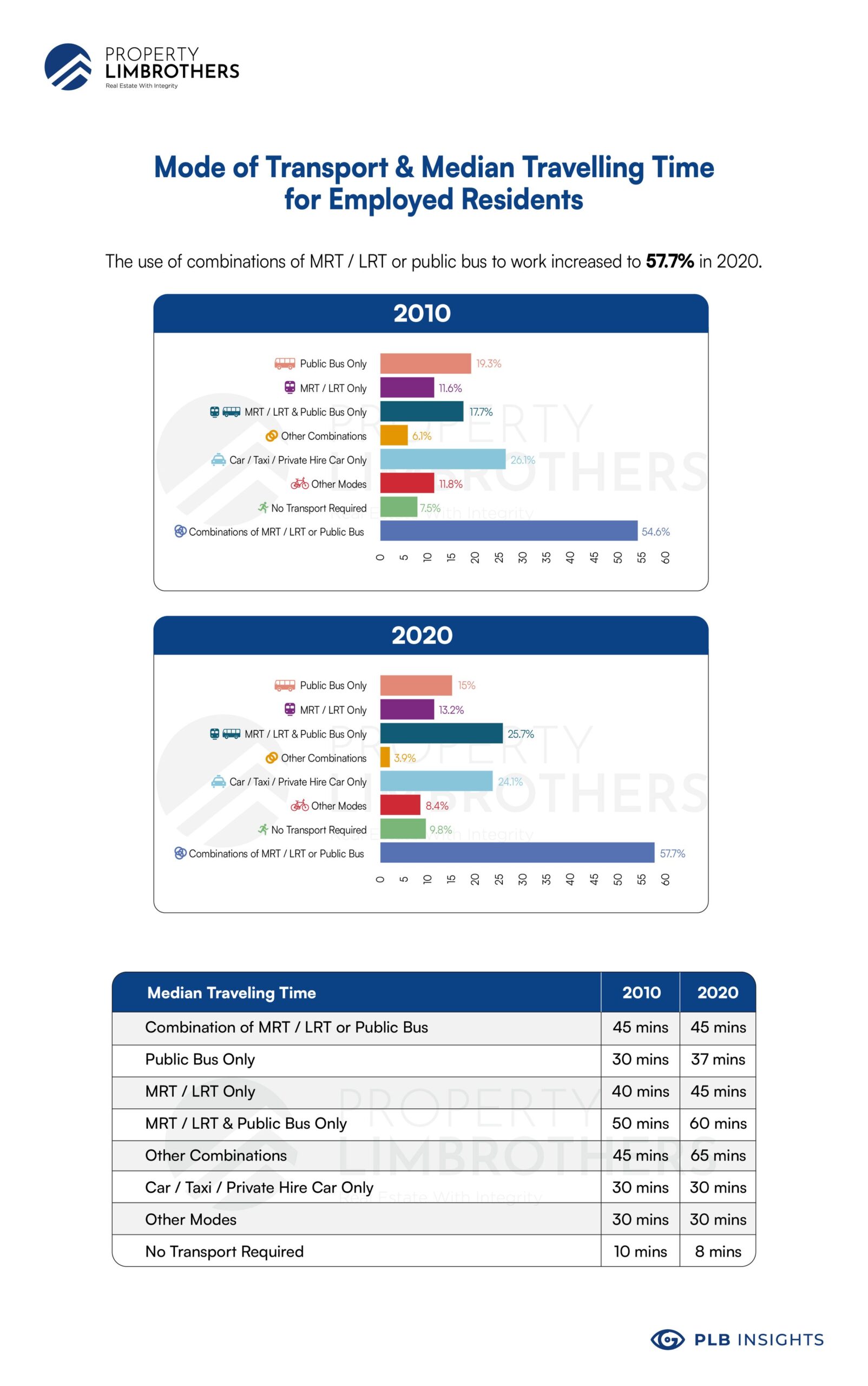

Increasing interconnectedness through expansion of Singapore’s Public Transport Infrastructure.

Singapore has been continuously working towards its aimed expansion of the MRT network to 360km by early 2030. With the new Thomson-East Coast line, which has already partially opened, and the Cross Island Line aimed to be completed by 2030, travelling in Singapore by public transport will become much quicker than it already is.

Not to mention it is definitely much cheaper than owning a car in Singapore. As a matter of fact, 57.7% of employed residents here took combinations of the bus, MRT, or LRT to work in 2020 – up from 54.6 per cent in 2010 according to the census conducted once every 10 years, which surveyed 150,000 households in 2020.

Changing Office Real Estate Landscape

Work From Home Arrangements

COVID-19 situation has accelerated remote teaching and online learning.

Businesses are reducing their office real estate as work seems to be able to take place productively even without a physical office — online. It would only make economic sense for companies to downsize office space to save capital expenditure on real estate. This, in turn, can be translated into bigger budgets in other segments of the company, such as research and development.

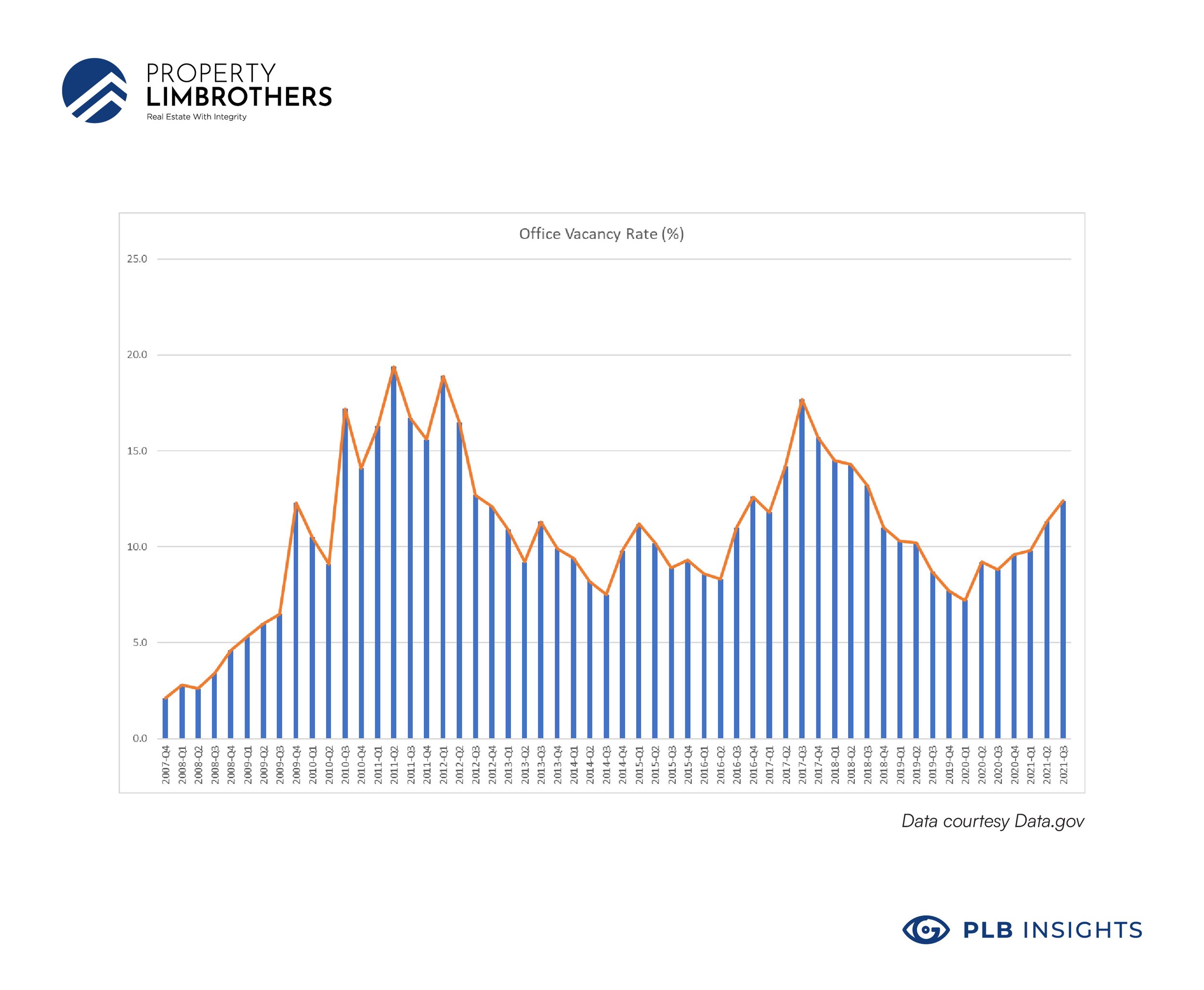

Office space vacancy is on the rise and will further increase; large landlords such as Capitaland are changing their vacant office space into co-working spaces but are still looking for users.

Increasing “Work from home” arrangements reduces foreigners relocating to Singapore hence reducing demand for residential rentals and demand for CCR.

Technology for video conferencing and remote work such as Zoom and Google Drive has been around for several years. However, it was only recently where COVID-19 had forced many of us to integrate these tools into our daily workflow. It has resulted in many business professionals realising that they can be more productive working remotely. On top of saving commute time and expenses, which companies can reallocate for more productive uses.

Although not all companies will have all their employees work remotely, it would be fair to say that all companies will at least rethink their corporate real estate to reduce the number and time employees work in the offices that are most often found in CCR regions.

The advent and pick up Co-Working spaces.

Co-working spaces have proliferated in the last few years and are expected to grow further. Co-working spaces are autonomous spaces where people can work independently (for different objectives or for different companies). The people in the environment generally do not work for the same company. These spaces are often found outside of areas designated for office use.

A report by Colliers suggests that coworking spaces now take up 3.7 million square feet (sq ft) in net lettable area (NLA) of Singapore’s commercial space, tripling from 1.2 million sq ft in 2015 to become one of the top six occupier sectors.

For example, WeWork in Singapore has grown over the years to have 14 sizable locations in Singapore. The National Library Board has also set up Smart Work Centres, which are co-working spaces in public libraries. The pay-per-use workspaces are equipped with meeting rooms, video conferencing facilities, Wi-Fi and photocopiers.

Even cafes and hotels are jumping on the bandwagon of co-working spaces — Orchard Hotel and Furama Riverfront are among those offering their lounges and high tea areas for people to pay by the hours to work.

Because of the aforementioned trends, it is no surprise that traditional office vacancy rates in CCR have been lingering higher and higher — closely reflecting the similar levels last seen during the Lehman economic recession.

So who is flocking to the city fringe?

As mentioned earlier, it is now the case that Singaporeans make up the majority of the property transactions. Most Singaporean buyers are still quantum-sensitive but appreciate a larger unit. Hence, bringing their attention to explore the RCR and OCR region for a budget-conscious purchase while still getting a slice of the luxury pie.

We. Want. More. Space!

There has been a shift in preferences for lifestyle in Singaporeans as families look to utilise the space in the homes and communities more as opposed to travelling overseas for leisure.

Singaporeans are now looking at getting more bedrooms and ground floor units for outdoor patio spaces (which previously only used to be appreciated by a niche group of homeowners). As is the case with getting penthouses and landed homes.

It is not surprising that people want more breathing space in their daily lives amidst this global pandemic. It has shifted Singaporeans’ habits from once going out or travelling overseas for fun to remaining at home to enjoy the luxuries that their property can offer.

As we work from home, study from home and generally spend more time at home. There is a natural greater appreciation for wanting more space.

URA Realis data showed that sales of large condominiums measuring at least 1,200 sq ft surged 205.5% to 4,335 units (including sub-sales) during the first half of 2021 from 1,419 units over the same period last year.

The figure surpassed the 2,056 units shifted over the same period in 2019 before the pandemic, and the 3,786 units transacted in the same period in 2018 before the introduction of cooling measures.

This is especially the case in RCR and OCR regions, where buyers tend to be buyer-occupants, although evident across all market segments.

As seen from the transaction data on properties of 1200 sq ft and above

-

there has been a 116% increase in transaction volume of properties 1200 sq ft and above since 2019

-

the total of 6234 units of 1200 sq ft transacted in 2021 trumps the total of 4881 in 2017

This is also further supported by data on property under 1200 sq ft

-

Properties under 1200 sq ft have only seen a 52% increase since 2019. This is underwhelming in comparison to the growth in the transaction of properties of 1200Sq ft and above

What will Singapore’s Real Estate Look Like in the future?

It should not surprise that Singapore has to build and rebuild itself constantly. We have to regularly upgrade infrastructure to remain relevant due to lack of space. Singapore state owns more than 80% of all land leased out according to a master plan — making it more possible to upgrade infrastructure constantly.

Integrated and Mixed-Use developments

A trend that is picking up is integrated and mixed-use developments, for example, One Holland Village Residences, which has been increasing in their allure due to greater convenience.

Mixed-use developments are an urban development strategy that blends residential and commercial spaces on a single plot of land.

Integrated Developments refer to a form of mixed-use developments which also have direct access to public infrastructure facilities such as MRT stations and/or Bus interchanges.

With the growing demand for integrated and mixed-use developments, their ability as Real Estate that reduces the need for travel will then also reduce the demand for living in the CCR region, supporting the trend of homebuyers shifting their attention from the central to city fringe homes!

In an alternate perspective, with the decentralization of the CBD being poised as one of URA’s priority in the coming decade, more commercial compounds would be repurposed for additional residential supply. The additional supply and new developments in the CBD would likely interest those that are on the hunt for the cosmopolitan living within the tall concrete jungle.

So is this demand shift permanent? And What does this mean for Home Owners and Home Buyers?

With space coming at a premium in Singapore’s limited land space, I think it is fair to say that the attention shift from central to city fringe homes is here to stay even when COVID-19 becomes a page in the history books.

It will be exciting how this demand changes for both RCR and CCR will further affect pricing in both the RCR and CCR region.

For those looking to jump on this bandwagon, do look out for the pitfalls of the newly implemented cooling measures that came late last year as a “Christmas present”, which you can read on our report here!

However, if you’re still unsure how to go about purchasing your next home, be it in the RCR or CCR region, do feel free to reach out to our buyer’s consultation team!

When you engage PropertyLimBrothers for your property transactions or investments, be assured that you have an entire team committed to doing its best as our team treats every transaction as if it were our own!

Click here to contact us now!