Sometimes, when we focus on the nitty-gritty of our daily lives – we tend to ignore the bigger picture. We disregard the larger financial issues and fail to appreciate situations with more financial significance.

More specifically, have you put in enough thought towards how you are financing your current property with your monthly payments? Or is it something that you have stored at the back of your mind? With poor planning, do you know that you could potentially lose $100k unknowingly?

The Cost of Financing Your Home With CPF Monies

The majority of Singaporean homeowners opt to pay for their homes via monies withdrawn from their CPF Ordinary Account (OA). By utilising the CPF OA, you are essentially “borrowing” your future retirement monies at a rate of 2.50% per annum – this is because you will need to refund the amount used with the accrued interest when you sell or transfer the property. If you are staying in a HDB, it is also likely that you might have taken up a HDB loan that comes at an interest rate of 2.60%.

Hence, there are two main costs to consider:

-

The 2.60% financing cost of the HDB loan

-

Opportunity cost of a 2.50% guaranteed returns from your CPF OA

Let’s explore what these numbers mean.

Financing Cost of HDB Loan

To facilitate understanding, let us make some assumptions here:

-

You are buying a $450k HDB flat

-

You used $50k from your CPF OA for the initial downpayment

-

You then took a $400k HDB loan at an interest rate of 2.60%

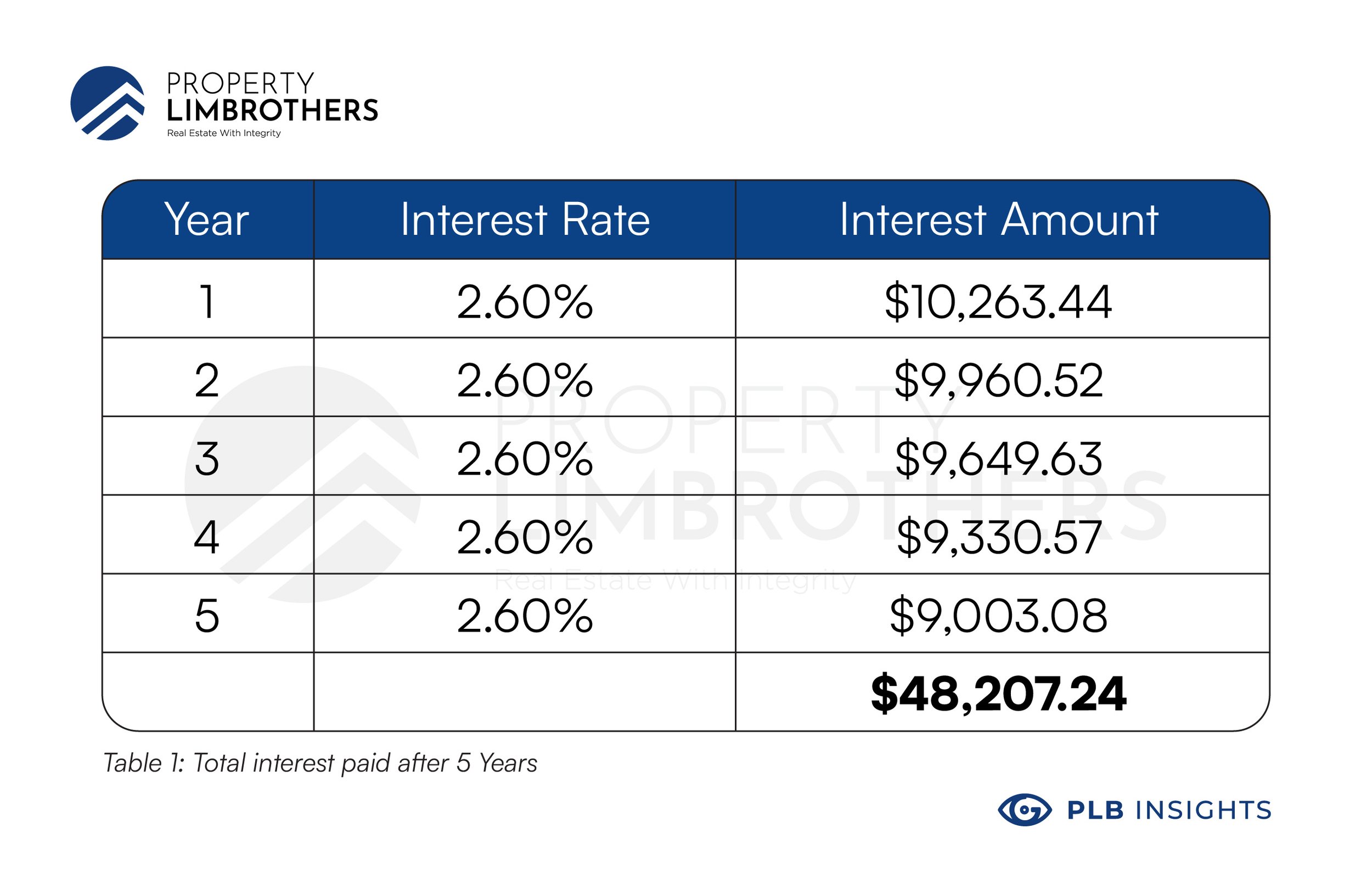

The total financing interest (from HDB Loan) that you would have paid at the end of 5 years would be approximately $48k.

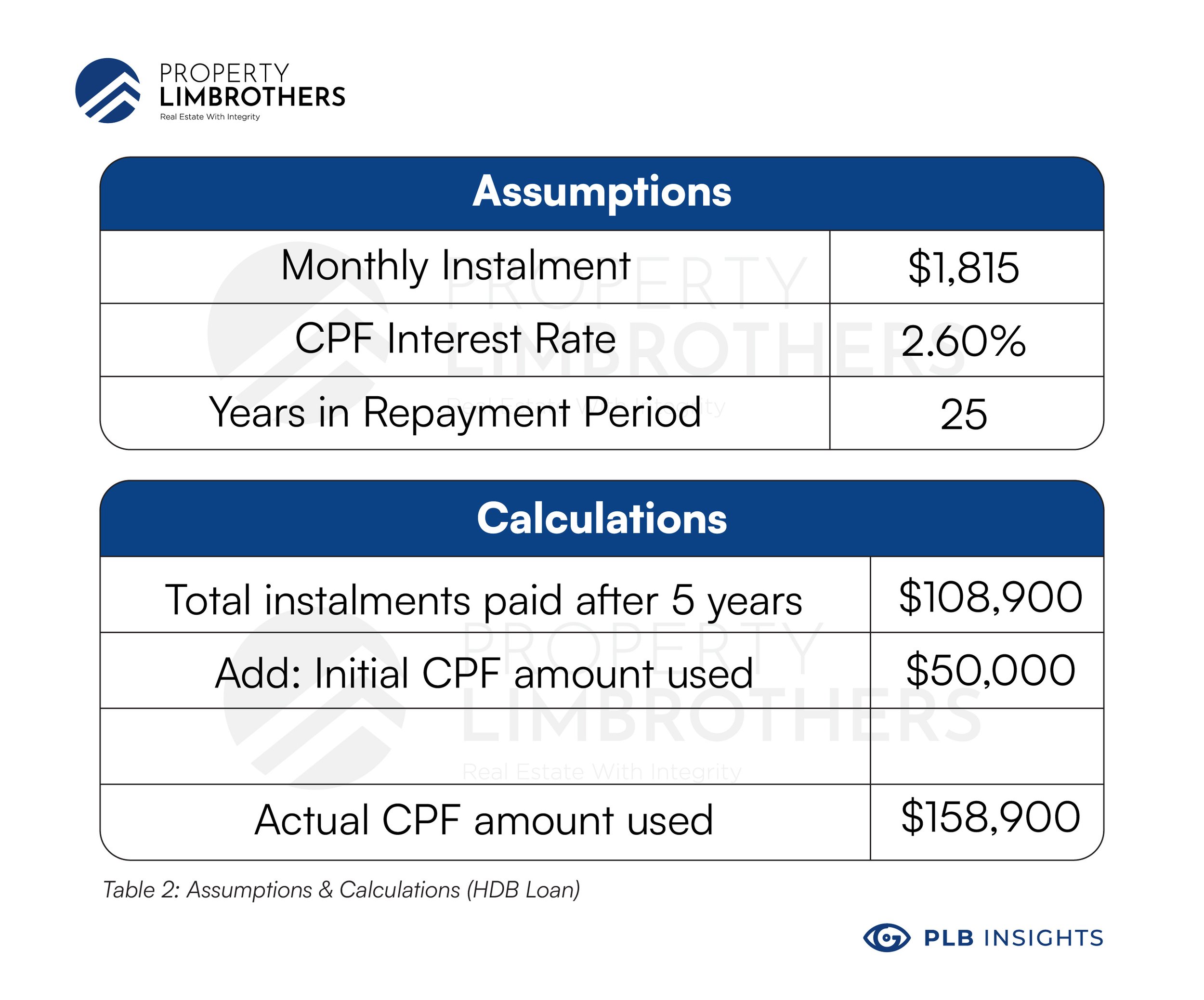

The total monthly installment of a $400k HDB loan is $1,815. Assuming this is to be deducted from your CPF OA every month, this means you are “borrowing” from your CPF OA an annual amount of $21,780. After 5 years, you would have withdrawn $108,900 ($21,780/Year x 5 Years) from your CPF OA.

Adding the $50k CPF monies used upfront, the actual CPF amount used will be $158,900.

CPF Accrued Interest

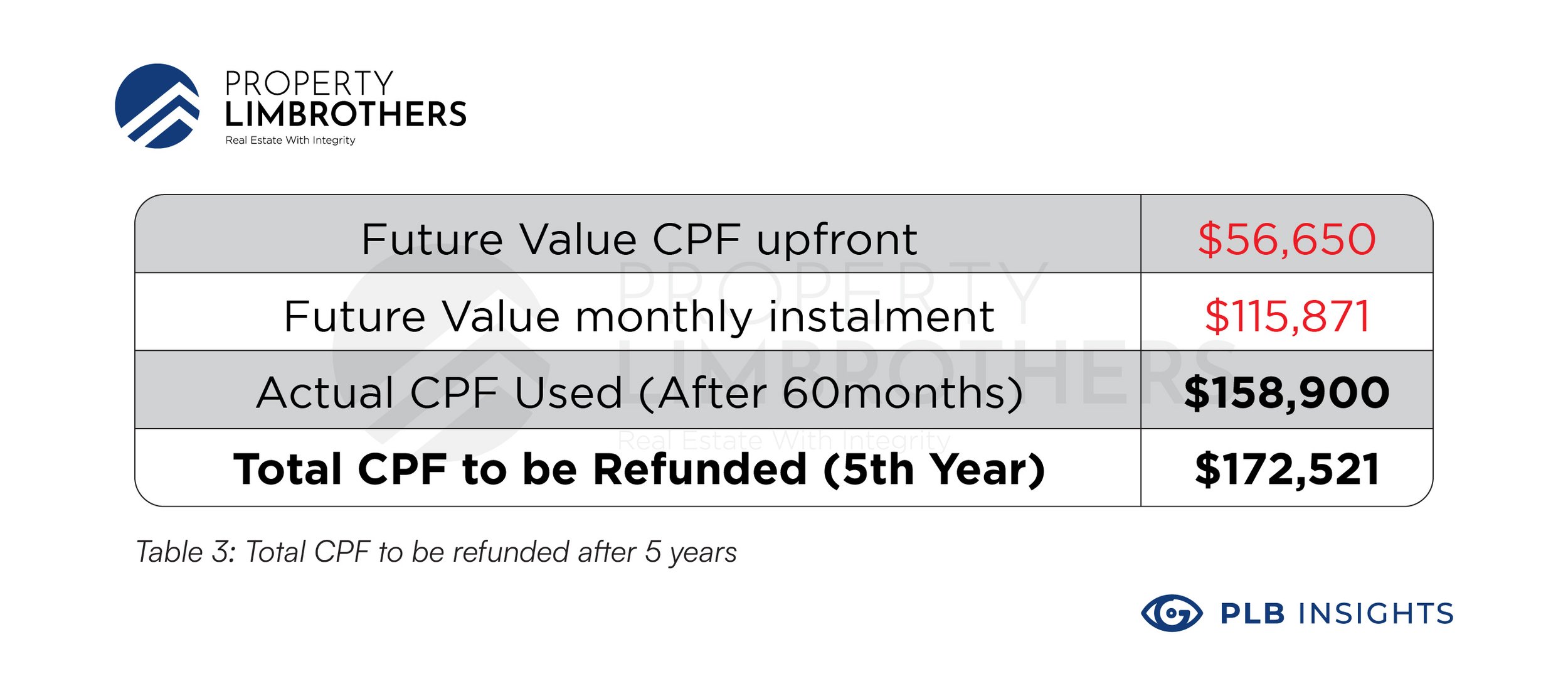

Including the accrued interest that you would have otherwise earned from your CPF OA if you had not utilised your CPF funds, the total amount to be refunded back to your CPF account will be $172,521.

This means that at the end of the five-year mark, the CPF accrued interest will be about $14k.

So in all, you will be bearing about $62k in the costs of owning your HDB flat after five years ($48k from HDB loan interest + $14k from CPF accrued interest).

Opportunity Cost from Compounding Effect

Let us also keep in mind the power of compounding interest.

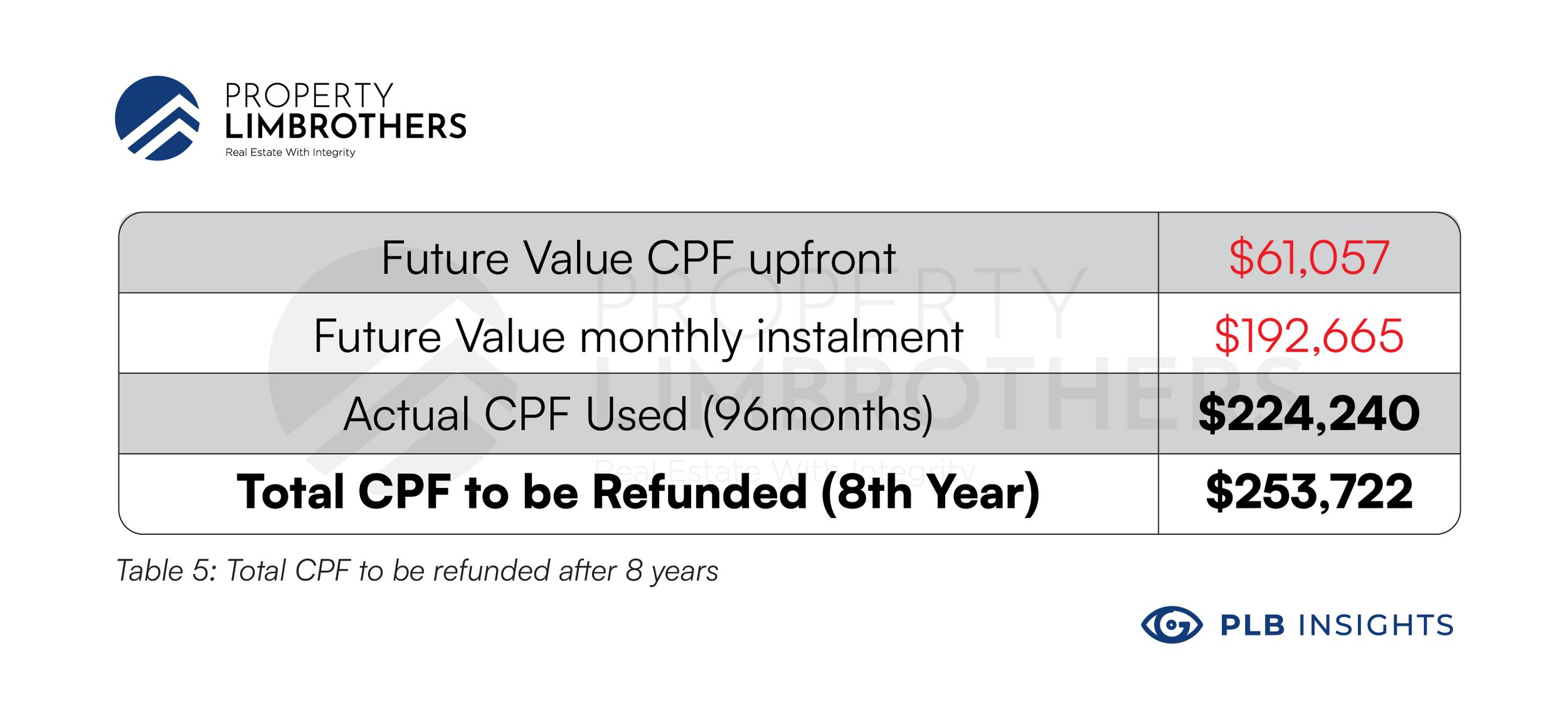

At the 8th year mark, the estimated costs will have ballooned to as follows:

-

Estimated accrued interest after eight years will be around $30k

-

Estimated total loan interest paid after eight years based on 2.60% interest rate will be around $73k

Thus, the total costs would have then increased to $103K upon the 8th year mark.

That is how you would have lost about $100k unknowingly through eight years of home ownership in Singapore.

However, do take note that numbers will differ based on the cost of your HDB flat and loan size. The best way to check your CPF accrued interest is to login to your CPF account and add up both yours and your spouse’s numbers.

If we were to go even more in-depth, there are actually two more hidden costs that most people will never pay attention to.

The Invisible Costs of Depreciation & Inflation

Depreciation

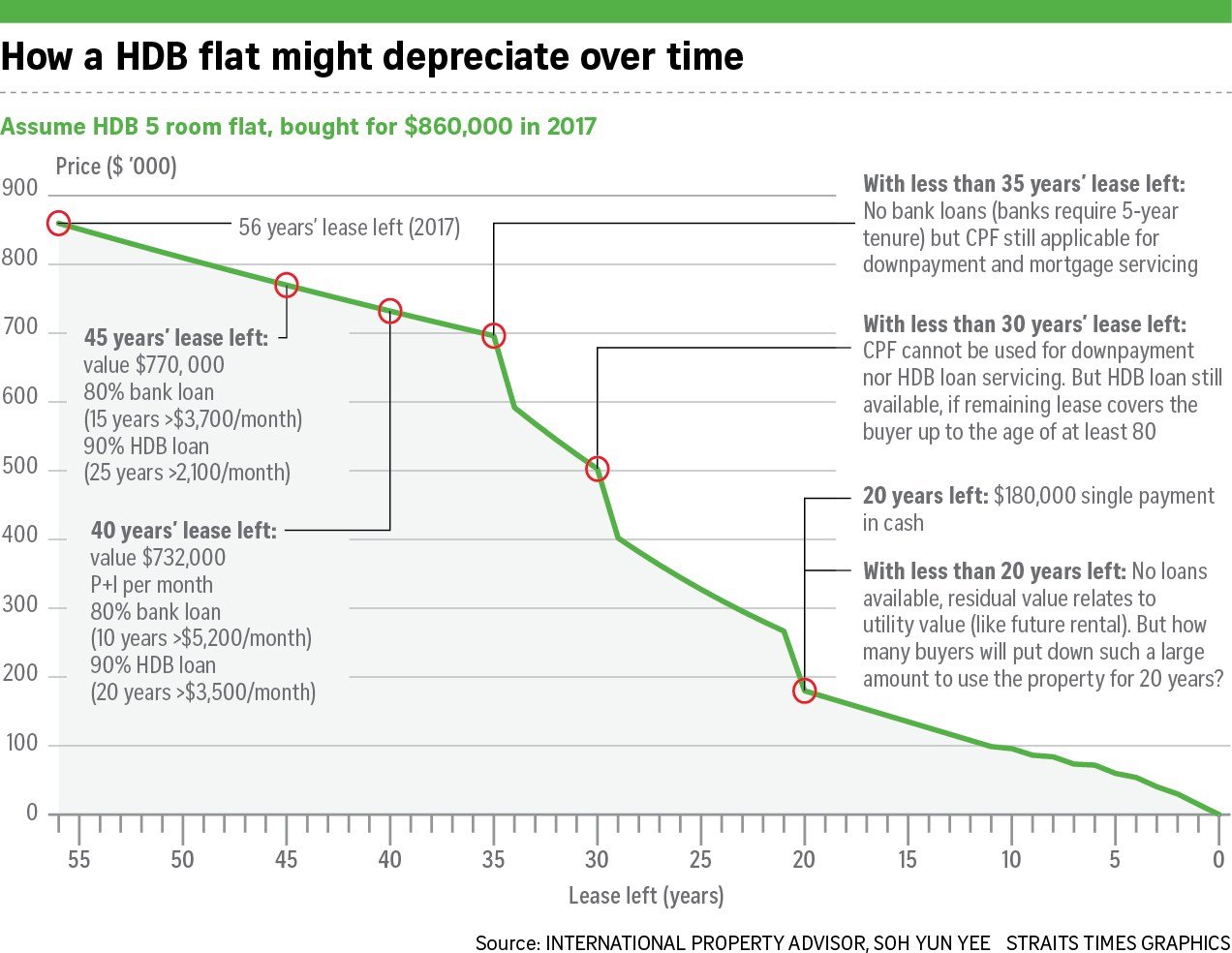

At some point in the future, a property is expected to depreciate in value as it ages. This is especially true for HDB flats that have crossed the 10 years mark (see table below).

It also becomes less sought-after as buyers tend to prefer newer properties – this is very evident in the way potential buyers would enquire about the remaining lease of the properties that we market.

Courtesy The Straits Times

Inflation

The average inflation rate in Singapore is about 2% per year.

While inflation can pull prices up – it becomes a problem when the property we own stagnates in price or depreciates instead.

Conversely, inflation can work for you and will be towards your benefit if you have parked your monies in the right property that appreciates along with inflation.

Closing Thoughts

People are familiar with the idea of compound interest for investments. But no one really thinks about how debt compounds – and this is the reality of numbers which you have to accept.

Perhaps this $100k is an acceptable cost to you. However, if you are already managing your personal credit & daily finances well, it does not hurt to also take some time to focus on this aspect of financial planning – for this is where you might be able to shift the needle significantly to help you achieve your financial goals!

We hope that this piece has given you some idea on the costs behind property ownership in Singapore, and how you may possibly reduce those costs to your advantage. Should you need guidance and professional advice, feel free to get in touch with the PropertyLimBrothers team, and we will get back to you shortly! In the meantime, take care and do keep a lookout for our next article!